Yahoo Finance

Yahoo Finance How Much Are Americans Spending on Financial Vices?

The Americans who can least afford it are spending the highest percentage of their income on what the folks at Bankrate describe as "financial vices." People in the lowest income bracket -- those earning under $30,000 a year -- spend "an average of $2,118 annually on restaurant food, prepared drinks (such as such as coffee, tea, and smoothies) and lottery tickets," according to the new Bankrate.com survey.

For these lower-income households, that adds up to 13% of their total income going toward such expenses. By contrast, the highest-earning category of households -- those annual incomes of at least $75,000 -- spend only 2.6% of their income on the same categories.

Lottery tickets are an especially dangerous financial vice. Image source: Getty Images.

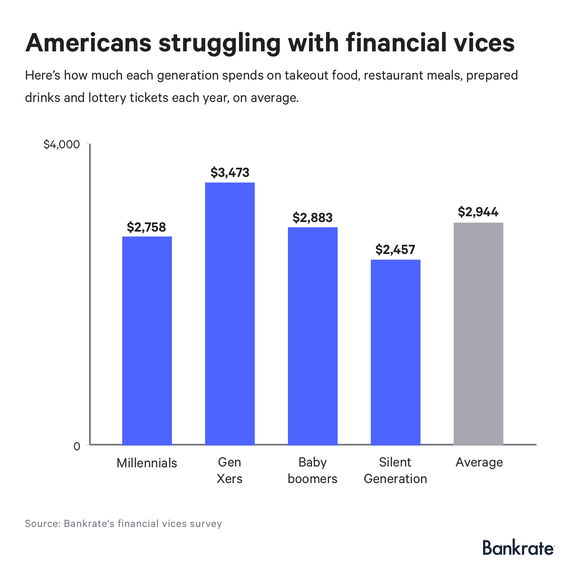

How is the money being spent?

Americans in general like to eat out. In fact, the bulk of so-called "vice" spending goes toward eating in restaurants or ordering takeout. The average American spends $2,443 a year on restaurant food, and 38% of us eat out at least three times a week, according to Bankrate.

Vice, of course, is relative to your specific financial situation. There are high-earners in poor financial shape who should cut back on the lattes and restaurant meals. There are also people who earn less but have made choices that put them in a position where they can afford to splurge a bit.

People do have to eat, however, and while it generally costs more to eat out than to cook at home, eating certainly isn't a completely frivolous expense. Buying lottery tickets is, however, and 28% of Americans in the lowest-income demographic play the lottery at least once a week, compared to 19% who earn more than $30,000 annually.

Low-income households spend an average of $412 each year on lottery tickets. Households earning at least $75,000 per year spend an average of $105 per year on lottery tickets.

"People who are struggling to make ends meet need to be extra careful about how they spend their money," said Bankrate.com analyst Amanda Dixon."The idea of striking it rich by winning the lottery is enticing, but you can earn a guaranteed return by putting the money in a high yield savings account."

Image source: Bankrate.

It takes discipline

It's easy to choose short-term convenience over longer-term financial security. That's true across all economic classes, but those decisions can be especially detrimental to lower-income households.

"For the average American, a few thousand dollars may not sound like a lot to spend each year on dining out and other financial vices," said Dixon. "However, if a Gen Xer was to invest that $3,473 a year for 10 years at an 8% return, they would end up with just over $50,000 that could go toward their retirement savings or their child's college fund."

It's important to save money, and creating an emergency fund should be among your first priorities. It's generally recommended that people have enough set aside to cover six months worth of their household expenses, to be deployed in case of large unexpected bills, job loss, health crises, and other serious financial issues.

Building such a reserve isn't a simple task, but it can be done incrementally by making small smart choices. Stop playing the lottery -- your odds of winning are astronomically bad. Cut back on eating out, and brew your own morning coffee. And realize that making these sacrifices now can put you on the path to a better financial future.

More From The Motley Fool

The Motley Fool has a disclosure policy.