Yahoo Finance

Yahoo Finance McCormick (MKC) Q4 Earnings & Sales Miss Estimates, Decline Y/Y

McCormick & Company, Incorporated MKC reported soft fourth-quarter fiscal 2022 results as both the top and bottom lines declined year over year and missed the Zacks Consensus Estimate. Results were impacted by the Kitchen Basics divestiture, reduced consumption in China due to the pandemic and cost inflation, among other factors.

However, the company is on track to capitalize on a sustained shift to cooking more at home, higher digital engagement, clean and flavorful eating and trusted brands.

Quarter in Detail

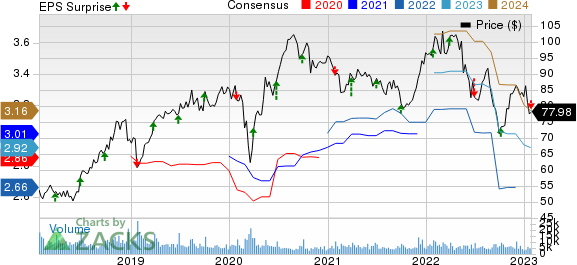

Adjusted earnings of 73 cents per share declined from 84 cents in the year-ago quarter. The metric also fell short of the Zacks Consensus Estimate of 86 cents per share.

McCormick & Company, Incorporated Price, Consensus and EPS Surprise

McCormick & Company, Incorporated price-consensus-eps-surprise-chart | McCormick & Company, Incorporated Quote

This global leader in flavor generated sales of $1,695.7 million, down 2% year over year. Constant-currency (cc) sales increased 2% on 9% growth from pricing actions, somewhat offset by a 3% decline in volumes.

The volume decline stemmed from the Kitchen Basics divestiture, reduced consumption in China due to the pandemic, the exit of a low-margin business across India and the Consumer business in Russia and a 4% decline from all other volumes and product mix. The top line missed the Zacks Consensus Estimate of $1,760 million.

During the quarter, cc sales increased at a three-year CAGR of 5%, relative to the pre-pandemic baseline of 2019. MKC’s adjusted gross profit margin contracted 410 basis points due to escalated cost inflation, higher other supply-chain expenses and an adverse product mix. These were somewhat countered by cost savings from the Comprehensive Continuous Improvement program and pricing actions.

The operating income was $264 million, down from the $276 million reported in the year-ago quarter. The downside was caused by gross margin contraction, mainly in the Flavor Solutions unit. The adjusted operating income fell from $309 million to $278 million.

Segment Details

Consumer: Sales went down 8% to $1,037.8 million, and cc sales fell 4% due to soft volumes and mix. These were somewhat compensated by pricing actions across all three regions.

The volume decline included the adverse impacts of the Kitchen Basics divestiture, reduced consumption in China due to the pandemic, and the exit of a low-margin business across India and the Consumer business in Russia. Sales dropped 4% in the Americas, 13% in the EMEA and 29% in Asia/Pacific.

Flavor Solutions: Sales in the segment advanced 9% to $657.9 million. On a cc basis, sales grew 14% due to solid pricing actions, improved volumes and a product mix.

Flavor Solutions sales in the Americas grew 13%. Flavor Solutions sales in the EMEA fell by 2%. Sales in the Asia/Pacific market remained flat year over year.

Financial Update

McCormick exited the quarter with cash and cash equivalents of $334 million, long-term debt of $3,642.3 million and total shareholders’ equity of $4,680.5 million. For the 12 months ended Nov 30, 2022, net cash provided by operating activities amounted to $651.5 million.

Fiscal 2023 Guidance

McCormick anticipates fiscal 2023 to witness a solid underlying business performance, backed by sales growth. It expects the Global Operating Effectiveness Program and the lapping of pandemic-led hurdles to have a positive effect on the fiscal 2023 operating income, which is likely to be somewhat negated by the impacts of the Kitchen Basics divestiture and a rise in employee incentive compensation costs.

Management anticipates currency movements to have a minimal impact on fiscal 2023 net sales, operating income and earnings per share (EPS).

For fiscal 2023, net sales are expected to increase 5-7% from the fiscal 2022 levels. Management expects sales growth to be fueled by pricing actions, which, along with cost savings, is likely to help it counter inflationary headwinds. The company anticipates seeing solid growth via brand strength, brand marketing, new products, category management and differentiated customer engagement.

The adjusted operating income is likely to grow 9-11%. Management envisions adjusted EPS in the band of $2.63-$2.68 in fiscal 2023.

The company expects adjusted earnings in the band of $2.56-$2.61 per share in fiscal 2023, suggesting 1-3% growth. The bottom line is likely to be fueled by a solid operating performance, partly offset by increased interest expenses and a higher projected adjusted effective tax rate.

This Zacks Rank #4 (Sell) stock has tumbled 8.6% in the past six months compared to the industry’s 3% increase.

Solid Consumer Staple Picks

Some better-ranked consumer staple stocks are e.l.f. Beauty, Inc. ELF, Conagra Brands CAG and Lamb Weston LW.

e.l.f. Beauty, which provides cosmetic and skin care products, currently sports a Zacks Rank #1 (Strong Buy). ELF has a trailing four-quarter earnings surprise of 92.8%, on average. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for e.l.f. Beauty’s current fiscal-year sales and EPS suggests an increase of 24.8% and 33.3%, respectively, from the year-ago reported number.

Conagra, a consumer-packaged goods food company, currently sports a Zacks Rank #1. CAG has a trailing four-quarter earnings surprise of 8.9%, on average.

The Zacks Consensus Estimate for Conagra’s current fiscal-year sales and earnings suggests growth of 6.8% and 11.9%, respectively, from the corresponding year-ago reported figures.

Lamb Weston, which is a frozen potato product company, currently sports a Zacks Rank #1. LW has a trailing four-quarter earnings surprise of 52.6%, on average.

The Zacks Consensus Estimate for Lamb Weston’s current fiscal-year sales and EPS suggests an increase of 19.5% and 89.9%, respectively, from the year-ago reported number.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Conagra Brands (CAG) : Free Stock Analysis Report

McCormick & Company, Incorporated (MKC) : Free Stock Analysis Report

e.l.f. Beauty (ELF) : Free Stock Analysis Report

Lamb Weston (LW) : Free Stock Analysis Report