Yahoo Finance

Yahoo Finance M&T Bank (MTB) Thrives on Organic Growth Amid Rising Costs

M&T Bank Corporation MTB continues to benefit from solid top-line growth, strategic acquisitions, and rising loan and deposit balances. However, increasing expenses and deteriorating credit quality are major concerns.

M&T Bank is focused on its organic growth and has shown remarkable revenue performance over the past few years. Additionally, the company’s operations as a solid and sustainable regional bank franchise with a footprint that spans six Mid-Atlantic States, as well as Washington, D.C., is another advantage. With a favorable lending scenario and high interest rates environment, the company’s net interest income is likely to aid revenue growth. Additionally, efforts to bolster non-interest income will further support the top line in the upcoming period.

M&T Bank has a solid balance sheet position. The company has witnessed solid growth in its deposits over the past few years. The bank is actively trying to acquire the industry's best deposit franchise. Its deposits are well-diversified in terms of clients and offerings. Additionally, MTB is also focused on growing its loan balances. In 2022, the bank acquired People’s United, which increased M&T Bank’s loans by $36 billion and deposits by $53 billion. We expect average loans and leases, net of unearned discount as well as total deposits to witness a three-year (2023-2026) CAGR of 4.6% and 3%, respectively.

M&T Bank maintains steady capital distribution activities. In May 2024, the company hiked its quarterly dividends by 4% to $1.35 per share, following an 8.3% increase in February 2023.

As of Mar 31, 2024, the company has a total debt (comprising short-term and long-term borrowings) of $16.25 billion, which was significantly lower than the cash and due from banks as well as interest-bearing deposits at banks of $33.84 billion. Given the company’s strong liquid profile and favorable debt-to-equity ratio, its capital distribution activities seem sustainable.

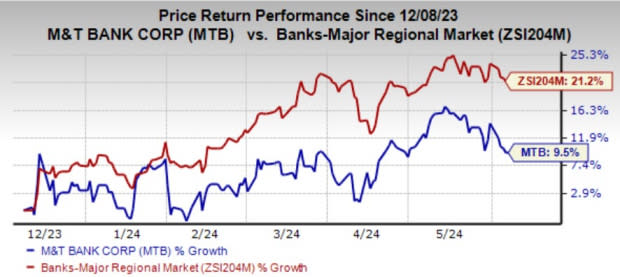

MTB currently carries a Zacks Rank #3 (Hold). Shares of the company have gained 9.5% over the past six months compared with the industry’s growth of 21.2%.

Image Source: Zacks Investment Research

However, MTB’s expenses have been escalating over the past few years. The rise was mainly attributable to the acquisition of People’s United. Going forward, the expense base is anticipated to remain elevated as the company continues to invest in strengthening its franchise. Management expects expenses (including intangible amortization) in the range of $5.25-$5.30 billion in 2024.

Deteriorating credit quality is a major headwind for M&T Bank. While the company recorded a recapture of provision for credit losses in 2021, it built substantial reserves over the past few years. We expect provision for credit losses to rise 7.9% in the current year. Further, non-performing assets and net-charge-off also witnessed an upward trend in the last few years. Given the concerns related to the expected economic slowdown, credit quality is likely to remain under pressure in the near term.

Stocks to Consider

Some better-ranked stocks from the finance space are First Financial Bancorp. FFBC and Bank of America Corporation BAC.

FFBC’s 2024 earnings estimates have increased 5.2% over the past 60 days. Shares of FFBC have lost 2.3% in the past three months. Currently, FFBC sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

BAC’s 2024 earnings estimates have risen 3.9% over the past 60 days. Shares of BAC have gained 28.2% over the past six months. At present, BAC carries a Zacks Rank #2 (Buy).

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Bank of America Corporation (BAC) : Free Stock Analysis Report

M&T Bank Corporation (MTB) : Free Stock Analysis Report

First Financial Bancorp. (FFBC) : Free Stock Analysis Report