Yahoo Finance

Yahoo Finance What We Learned About Volt Power Group's (ASX:VPR) CEO Pay

Adam Boyd is the CEO of Volt Power Group Limited (ASX:VPR), and in this article, we analyze the executive's compensation package with respect to the overall performance of the company. This analysis will also assess whether Volt Power Group pays its CEO appropriately, considering recent earnings growth and total shareholder returns.

Check out our latest analysis for Volt Power Group

How Does Total Compensation For Adam Boyd Compare With Other Companies In The Industry?

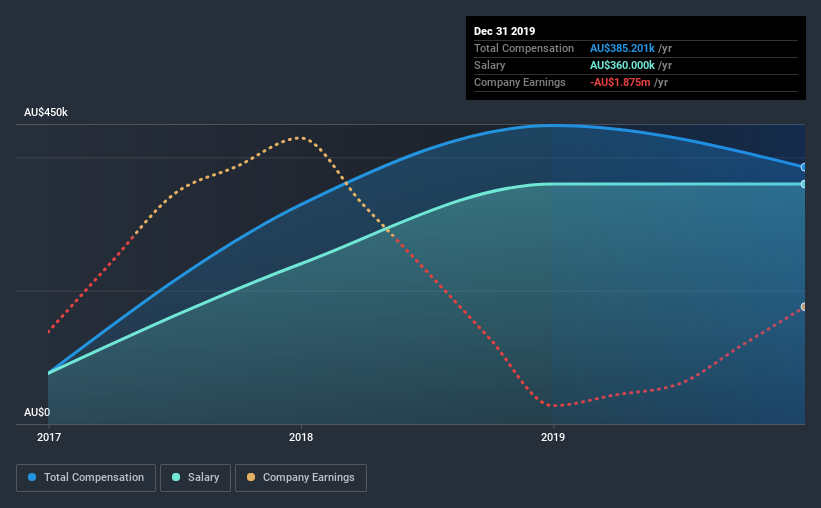

According to our data, Volt Power Group Limited has a market capitalization of AU$14m, and paid its CEO total annual compensation worth AU$385k over the year to December 2019. Notably, that's a decrease of 14% over the year before. In particular, the salary of AU$360.0k, makes up a huge portion of the total compensation being paid to the CEO.

In comparison with other companies in the industry with market capitalizations under AU$279m, the reported median total CEO compensation was AU$486k. So it looks like Volt Power Group compensates Adam Boyd in line with the median for the industry. Moreover, Adam Boyd also holds AU$1.6m worth of Volt Power Group stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

Component | 2019 | 2018 | Proportion (2019) |

Salary | AU$360k | AU$360k | 93% |

Other | AU$25k | AU$88k | 7% |

Total Compensation | AU$385k | AU$448k | 100% |

Speaking on an industry level, nearly 55% of total compensation represents salary, while the remainder of 45% is other remuneration. Volt Power Group pays out 93% of remuneration in the form of a salary, significantly higher than the industry average. If salary is the major component in total compensation, it suggests that the CEO receives a higher fixed proportion of the total compensation, regardless of performance.

A Look at Volt Power Group Limited's Growth Numbers

Volt Power Group Limited's earnings per share (EPS) grew 40% per year over the last three years. Its revenue is down 32% over the previous year.

Shareholders would be glad to know that the company has improved itself over the last few years. The lack of revenue growth isn't ideal, but it is the bottom line that counts most in business. While we don't have analyst forecasts for the company, shareholders might want to examine this detailed historical graph of earnings, revenue and cash flow.

Has Volt Power Group Limited Been A Good Investment?

With a three year total loss of 67% for the shareholders, Volt Power Group Limited would certainly have some dissatisfied shareholders. This suggests it would be unwise for the company to pay the CEO too generously.

To Conclude...

As previously discussed, Adam is compensated close to the median for companies of its size, and which belong to the same industry. At the same time, the company has logged negative shareholder returns over the last three years. However, earnings growth is positive over the same time frame. Overall, we wouldn't say Adam is paid an unjustified compensation, but shareholders might not favor a raise before shareholder returns show a positive trend.

We can learn a lot about a company by studying its CEO compensation trends, along with looking at other aspects of the business. We identified 4 warning signs for Volt Power Group (2 are concerning!) that you should be aware of before investing here.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.