Yahoo Finance

Yahoo Finance Investors in SiTime (NASDAQ:SITM) have made a incredible return of 585% over the past three years

Investing can be hard but the potential fo an individual stock to pay off big time inspires us. But when you hold the right stock for the right time period, the rewards can be truly huge. One such superstar is SiTime Corporation (NASDAQ:SITM), which saw its share price soar 585% in three years. It's also good to see the share price up 32% over the last quarter. The company reported its financial results recently; you can catch up on the latest numbers by reading our company report. It really delights us to see such great share price performance for investors.

So let's assess the underlying fundamentals over the last 3 years and see if they've moved in lock-step with shareholder returns.

View our latest analysis for SiTime

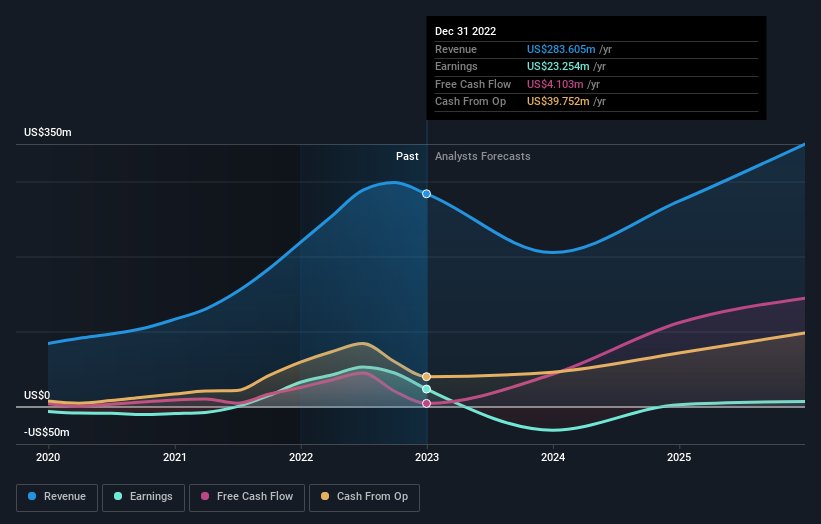

While SiTime made a small profit, in the last year, we think that the market is probably more focussed on the top line growth at the moment. As a general rule, we think this kind of company is more comparable to loss-making stocks, since the actual profit is so low. It would be hard to believe in a more profitable future without growing revenues.

In the last 3 years SiTime saw its revenue grow at 46% per year. That's well above most pre-profit companies. And it's not just the revenue that is taking off. The share price is up 90% per year in that time. It's always tempting to take profits after a share price gain like that, but high-growth companies like SiTime can sometimes sustain strong growth for many years. In fact, it might be time to put it on your watchlist, if you're not already familiar with the stock.

You can see how earnings and revenue have changed over time in the image below (click on the chart to see the exact values).

We know that SiTime has improved its bottom line over the last three years, but what does the future have in store? This free interactive report on SiTime's balance sheet strength is a great place to start, if you want to investigate the stock further.

A Different Perspective

The last twelve months weren't great for SiTime shares, which performed worse than the market, costing holders 45%. Meanwhile, the broader market slid about 11%, likely weighing on the stock. Investors are up over three years, booking 90% per year, much better than the more recent returns. Sometimes when a good quality long term winner has a weak period, it's turns out to be an opportunity, but you really need to be sure that the quality is there. It's always interesting to track share price performance over the longer term. But to understand SiTime better, we need to consider many other factors. Consider for instance, the ever-present spectre of investment risk. We've identified 4 warning signs with SiTime , and understanding them should be part of your investment process.

If you would prefer to check out another company -- one with potentially superior financials -- then do not miss this free list of companies that have proven they can grow earnings.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on American exchanges.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Join A Paid User Research Session

You’ll receive a US$30 Amazon Gift card for 1 hour of your time while helping us build better investing tools for the individual investors like yourself. Sign up here