Yahoo Finance

Yahoo Finance Investors in Northbridge Industrial Services (LON:NBI) have made a splendid return of 146% over the past year

When you buy shares in a company, there is always a risk that the price drops to zero. But if you pick the right business to buy shares in, you can make more than you can lose. For example, the Northbridge Industrial Services plc (LON:NBI) share price had more than doubled in just one year - up 146%. Also pleasing for shareholders was the 66% gain in the last three months. This could be related to the recent financial results, released recently - you can catch up on the most recent data by reading our company report. Having said that, the longer term returns aren't so impressive, with stock gaining just 27% in three years.

Let's take a look at the underlying fundamentals over the longer term, and see if they've been consistent with shareholders returns.

See our latest analysis for Northbridge Industrial Services

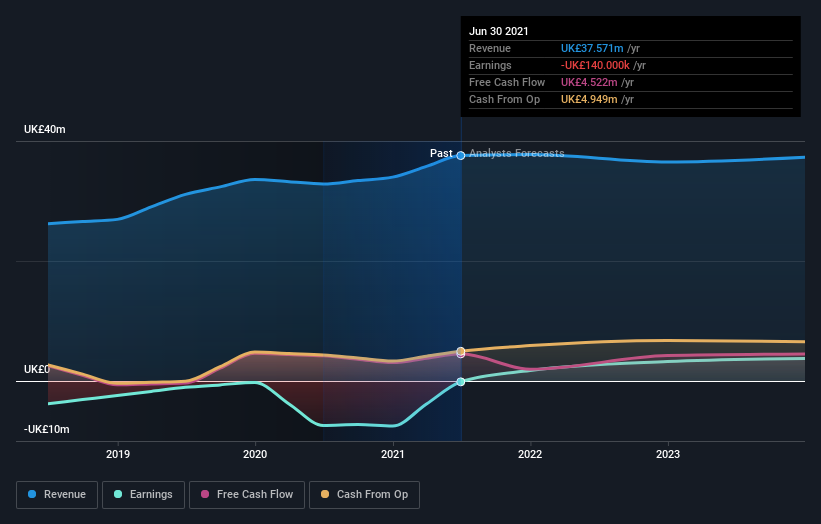

Northbridge Industrial Services wasn't profitable in the last twelve months, it is unlikely we'll see a strong correlation between its share price and its earnings per share (EPS). Arguably revenue is our next best option. Generally speaking, companies without profits are expected to grow revenue every year, and at a good clip. Some companies are willing to postpone profitability to grow revenue faster, but in that case one does expect good top-line growth.

In the last year Northbridge Industrial Services saw its revenue grow by 14%. That's a fairly respectable growth rate. While that revenue growth is pretty good the share price performance outshone it, with a lift of 146% as mentioned above. Given that the business has made good progress on the top line, it would be worth taking a look at its path to profitability. But investors need to be wary of how the 'fear of missing out' could influence them to buy without doing thorough research.

The image below shows how earnings and revenue have tracked over time (if you click on the image you can see greater detail).

Take a more thorough look at Northbridge Industrial Services' financial health with this free report on its balance sheet.

A Different Perspective

It's good to see that Northbridge Industrial Services has rewarded shareholders with a total shareholder return of 146% in the last twelve months. That's better than the annualised return of 12% over half a decade, implying that the company is doing better recently. Given the share price momentum remains strong, it might be worth taking a closer look at the stock, lest you miss an opportunity. While it is well worth considering the different impacts that market conditions can have on the share price, there are other factors that are even more important. Consider for instance, the ever-present spectre of investment risk. We've identified 3 warning signs with Northbridge Industrial Services , and understanding them should be part of your investment process.

If you are like me, then you will not want to miss this free list of growing companies that insiders are buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on GB exchanges.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.