Yahoo Finance

Yahoo Finance Intchains Group Limited's (NASDAQ:ICG) Popularity With Investors Is Under Threat From Overpricing

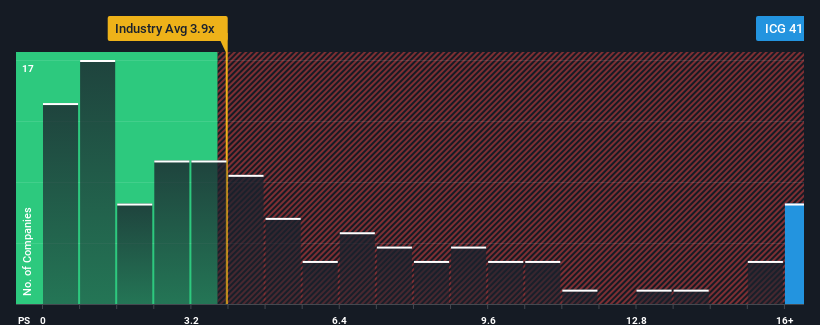

You may think that with a price-to-sales (or "P/S") ratio of 41.1x Intchains Group Limited (NASDAQ:ICG) is a stock to avoid completely, seeing as almost half of all the Semiconductor companies in the United States have P/S ratios under 3.9x and even P/S lower than 1.3x aren't out of the ordinary. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so lofty.

Check out our latest analysis for Intchains Group

How Has Intchains Group Performed Recently?

As an illustration, revenue has deteriorated at Intchains Group over the last year, which is not ideal at all. It might be that many expect the company to still outplay most other companies over the coming period, which has kept the P/S from collapsing. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on Intchains Group's earnings, revenue and cash flow.

Is There Enough Revenue Growth Forecasted For Intchains Group?

The only time you'd be truly comfortable seeing a P/S as steep as Intchains Group's is when the company's growth is on track to outshine the industry decidedly.

Retrospectively, the last year delivered a frustrating 89% decrease to the company's top line. Even so, admirably revenue has lifted 47% in aggregate from three years ago, notwithstanding the last 12 months. Accordingly, while they would have preferred to keep the run going, shareholders would definitely welcome the medium-term rates of revenue growth.

This is in contrast to the rest of the industry, which is expected to grow by 48% over the next year, materially higher than the company's recent medium-term annualised growth rates.

With this in mind, we find it worrying that Intchains Group's P/S exceeds that of its industry peers. It seems most investors are ignoring the fairly limited recent growth rates and are hoping for a turnaround in the company's business prospects. There's a good chance existing shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with recent growth rates.

The Bottom Line On Intchains Group's P/S

We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

The fact that Intchains Group currently trades on a higher P/S relative to the industry is an oddity, since its recent three-year growth is lower than the wider industry forecast. Right now we aren't comfortable with the high P/S as this revenue performance isn't likely to support such positive sentiment for long. Unless the recent medium-term conditions improve markedly, it's very challenging to accept these the share price as being reasonable.

A lot of potential risks can sit within a company's balance sheet. You can assess many of the main risks through our free balance sheet analysis for Intchains Group with six simple checks.

If you're unsure about the strength of Intchains Group's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.