Yahoo Finance

Yahoo Finance Independent Bank (NASDAQ:IBCP) Will Pay A Dividend Of $0.24

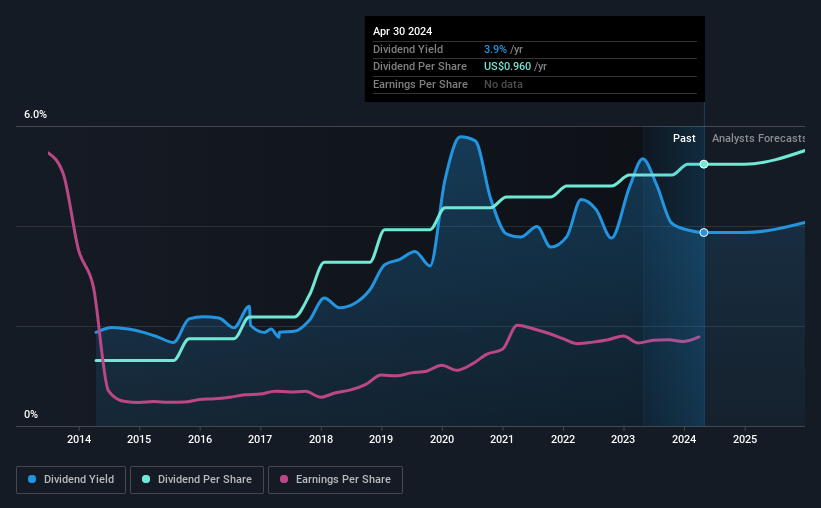

Independent Bank Corporation (NASDAQ:IBCP) has announced that it will pay a dividend of $0.24 per share on the 13th of May. Based on this payment, the dividend yield will be 3.9%, which is fairly typical for the industry.

See our latest analysis for Independent Bank

Independent Bank's Earnings Will Easily Cover The Distributions

We like a dividend to be consistent over the long term, so checking whether it is sustainable is important.

Independent Bank has established itself as a dividend paying company with over 10 years history of distributing earnings to shareholders. Past distributions do not necessarily guarantee future ones, but Independent Bank's payout ratio of 31% is a good sign as this means that earnings decently cover dividends.

Looking forward, earnings per share is forecast to fall by 0.7% over the next year. But if the dividend continues along the path it has been on recently, we estimate the future payout ratio could be 37%, which would be comfortable for the company to continue in the future.

Independent Bank Has A Solid Track Record

The company has an extended history of paying stable dividends. Since 2014, the dividend has gone from $0.24 total annually to $0.96. This implies that the company grew its distributions at a yearly rate of about 15% over that duration. We can see that payments have shown some very nice upward momentum without faltering, which provides some reassurance that future payments will also be reliable.

The Dividend Looks Likely To Grow

The company's investors will be pleased to have been receiving dividend income for some time. We are encouraged to see that Independent Bank has grown earnings per share at 12% per year over the past five years. A low payout ratio and decent growth suggests that the company is reinvesting well, and it also has plenty of room to increase the dividend over time.

We Really Like Independent Bank's Dividend

In summary, it is good to see that the dividend is staying consistent, and we don't think there is any reason to suspect this might change over the medium term. The distributions are easily covered by earnings, and there is plenty of cash being generated as well. However, it is worth noting that the earnings are expected to fall over the next year, which may not change the long term outlook, but could affect the dividend payment in the next 12 months. Taking this all into consideration, this looks like it could be a good dividend opportunity.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. As an example, we've identified 1 warning sign for Independent Bank that you should be aware of before investing. Is Independent Bank not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.