Yahoo Finance

Yahoo Finance Imagine Owning Prodigy Gold (ASX:PRX) And Trying To Stomach The 86% Share Price Drop

Long term investing is the way to go, but that doesn't mean you should hold every stock forever. It hits us in the gut when we see fellow investors suffer a loss. Anyone who held Prodigy Gold NL (ASX:PRX) for five years would be nursing their metaphorical wounds since the share price dropped 86% in that time. And we doubt long term believers are the only worried holders, since the stock price has declined 60% over the last twelve months. Shareholders have had an even rougher run lately, with the share price down 49% in the last 90 days. But this could be related to the weak market, which is down 24% in the same period.

We really hope anyone holding through that price crash has a diversified portfolio. Even when you lose money, you don't have to lose the lesson.

View our latest analysis for Prodigy Gold

With just AU$168,037 worth of revenue in twelve months, we don't think the market considers Prodigy Gold to have proven its business plan. This state of affairs suggests that venture capitalists won't provide funds on attractive terms. So it seems that the investors focused more on what could be, than paying attention to the current revenues (or lack thereof). It seems likely some shareholders believe that Prodigy Gold will find or develop a valuable new mine before too long.

As a general rule, if a company doesn't have much revenue, and it loses money, then it is a high risk investment. You should be aware that there is always a chance that this sort of company will need to issue more shares to raise money to continue pursuing its business plan. While some such companies go on to make revenue, profits, and generate value, others get hyped up by hopeful naifs before eventually going bankrupt. Prodigy Gold has already given some investors a taste of the bitter losses that high risk investing can cause.

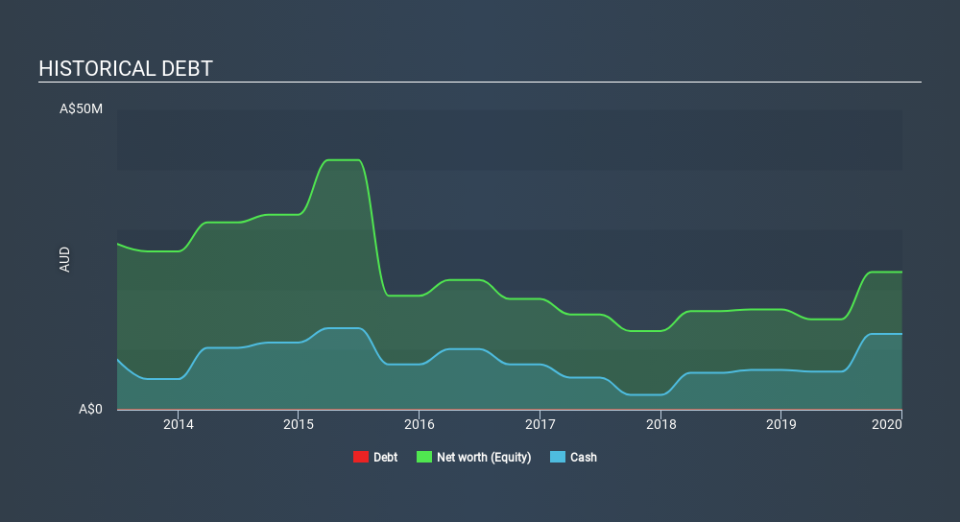

Prodigy Gold had cash in excess of all liabilities of AU$10m when it last reported (December 2019). That's not too bad but management may have to think about raising capital or taking on debt, unless the company is close to breaking even. We'd venture that shareholders are concerned about the need for more capital, because the share price has dropped 33% per year, over 5 years. The image below shows how Prodigy Gold's balance sheet has changed over time; if you want to see the precise values, simply click on the image.

It can be extremely risky to invest in a company that doesn't even have revenue. There's no way to know its value easily. What if insiders are ditching the stock hand over fist? I would feel more nervous about the company if that were so. You can click here to see if there are insiders selling.

A Different Perspective

We regret to report that Prodigy Gold shareholders are down 60% for the year. Unfortunately, that's worse than the broader market decline of 14%. Having said that, it's inevitable that some stocks will be oversold in a falling market. The key is to keep your eyes on the fundamental developments. Regrettably, last year's performance caps off a bad run, with the shareholders facing a total loss of 33% per year over five years. We realise that Baron Rothschild has said investors should "buy when there is blood on the streets", but we caution that investors should first be sure they are buying a high quality business. It's always interesting to track share price performance over the longer term. But to understand Prodigy Gold better, we need to consider many other factors. For example, we've discovered 5 warning signs for Prodigy Gold (1 can't be ignored!) that you should be aware of before investing here.

We will like Prodigy Gold better if we see some big insider buys. While we wait, check out this free list of growing companies with considerable, recent, insider buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on AU exchanges.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.