Yahoo Finance

Yahoo Finance Here's Why You Should Stay Invested in Chubb (CB) Stock

Chubb Limited CB is set to gain from its compelling portfolio, strong renewal retention, positive rate increases, strategic initiatives to fuel profitability and a solid capital position.

This insurer, carrying a Zacks Rank #3 (Hold) currently, has a decent history of delivering an earnings surprise in the last four reported quarters, the average being 23.44%.

Earnings of this insurer grew 19.4% in the last five years, better than the industry average of 10.4%. The expected long-term earnings growth rate is pegged at 2%.

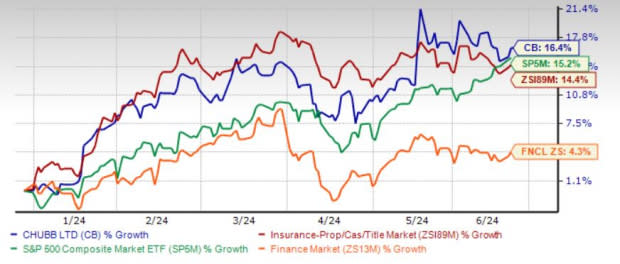

An Outperformer

Shares have gained 16.4% year to date, outperforming the industry’s 14.4% growth. The Finance sector and the S&P 500 Composite have grown 4.3% and 15.2%, respectively, in the said time frame.

Image Source: Zacks Investment Research

Return on Capital

Return on equity in the trailing 12 months was 16.3%, better than the industry average of 7.8%. Return on equity, a profitability measure, reflects how effectively a company is utilizing its shareholders.

Also, return on invested capital (ROIC) has been increasing over the last few quarters amid capital investments made over the same time frame. This reflects CB’s efficiency in utilizing funds to generate income. ROIC in the trailing 12 months was 10.5%, better than the industry average of 5.9%.

Growth Drivers

Focus on capitalizing on the potential of middle-market businesses (both domestic and international) and enhancing traditional core packages and specialty products bodes well for Chubb’s long-term growth. This apart, the insurer has also been making investments in various strategic initiatives. It is focusing on cyber insurance that has immense room for growth.

Chubb’s strategic mergers and acquisitions diversify its compelling portfolio, add capabilities and synergies and expand its geographic footprint. The addition of Cigna’s life and non-life insurance companies and the acquisition of a higher stake in Huatai Group, among others, bear testimony to the strategy.

Acquisitions have also improved premium revenues, the major component of the insurer’s top line. Premiums should also benefit from commercial P&C rate increases, new business and strong renewal retention.

Investment income continues to gain from improving operating cash flow coupled with a better rate environment. Management estimates investment income to be $1.45 billion in the second quarter of 2024 and grow thereafter.

Impressive Dividend History

Banking on operational expertise, Chubb boasts an impressive dividend history. It has increased dividends for 31 straight years. CB has a dividend yield of 1.3%, better than the industry average of 0.3%. This makes the stock an attractive pick for yield-seeking investors.

Risks

Despite the upside potential, there are a few factors that investors should keep an eye on. Chubb has substantial exposure to loss from natural disasters and man-made catastrophes, which have been inducing volatility in its underwriting profitability and pulling combined ratio.

Also, Chubb has been witnessing a noticeable increase in expenses, which weighs on margin expansion.

Stocks to Consider

Some top-ranked stocks from the insurance industry are HCI Group, Inc. HCI, Palomar Holdings PLMR and ProAssurance PRA. Each stock presently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

HCI Group’s earnings surpassed estimates in each of the last four quarters, the average beat being 139.15%. In the past year, shares of HCI have gained 7.8%.

The Zacks Consensus Estimate for HCI’s 2024 and 2025 earnings implies 57.6% and 4.3% year-over-year growth, respectively.

Palomar’s earnings surpassed estimates in each of the last four quarters, the average earnings surprise being 15.10%. In the past year, PLMR’s stock has surged 45%.

The Zacks Consensus Estimate for PLMR’s 2024 and 2025 earnings indicates 26% and 18% year-over-year growth, respectively.

ProAssurance earnings surpassed estimates in two of the last four quarters and missed in the other two. In the past year, PRA’s stock has lost 9.1%.

The Zacks Consensus Estimate for PRA’s 2024 and 2025 earnings implies 371.4% and 72.6% year-over-year growth, respectively.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Chubb Limited (CB) : Free Stock Analysis Report

ProAssurance Corporation (PRA) : Free Stock Analysis Report

HCI Group, Inc. (HCI) : Free Stock Analysis Report

Palomar Holdings, Inc. (PLMR) : Free Stock Analysis Report