Yahoo Finance

Yahoo Finance Here's Why You Should Retain Ralph Lauren (RL) Stock Now

Ralph Lauren Corporation RL seems to be in good shape, thanks to its sturdy strategic endeavors. The company has been making significant progress in expanding its digital and omnichannel capabilities through investments in mobile, omnichannel and fulfillment. Ralph Lauren’s “Next Great Chapter” plan appears encouraging too.

Let’s delve deeper.

Strategies in Detail

Ralph Lauren is expanding its connected retail capabilities, including virtual selling appointments, buy online, pick up in store, endless aisle product availability and more. The company has also launched its first-ever full catalog Ralph Lauren mobile app, thereby efficiently leveraging its connected retail capabilities to deliver the most personalized and content-rich platform.

Impressively, the company added more than 5 million new consumers to its direct-to-consumer business in fiscal 2024. Its followers on social media grew low double digits year over year to over 58 million, driven by TikTok, Instagram, Line and Douyin. Region-wise, digital sales were up 11% in Europe and 19% in Asia in fourth-quarter fiscal 2024.

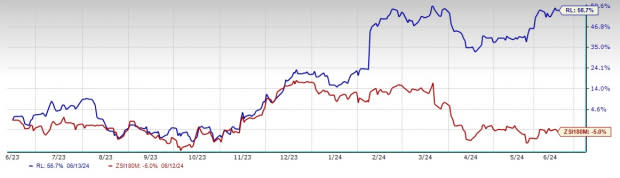

Image Source: Zacks Investment Research

The company remains focused on digital investments to continue the creation of content for all platforms, enhancing digital capabilities to improve the user experience and leveraging AI and data to serve its consumers more efficiently. During the fiscal year, RL witnessed solid direct-to-consumer comp growth apart from expanding its connected ecosystems across significant markets. Comps were up mid-single digits across both its brick-and-mortar stores and digital channels.

As part of the “Next Great Chapter” plan, the company has completed the transition of Chaps to a licensed business, thus concluding its portfolio realignment. This enables it to focus on core brands, as part of the “Next Great Chapter” elevation strategy. In addition, the company’s strategy of product elevation, personalized and targeted promotion, disciplined inventory management and favorable channel and geographic mix bode well.

However, Ralph Lauren has been witnessing a dismal performance across its North America segment’s wholesale channel for a while now. Higher promotions in the North America market and an unfavorable wholesale timing shift have been acting as deterrents.

Nevertheless, Ralph Lauren is optimistic about fiscal 2025. Management anticipates year-over-year revenue growth at constant currency in the low-single digits, revolving around 2-3%. It expects the operating margin to grow in the range of 100-120 basis points at constant currency on higher gross margin and leveraged operating expenses. The gross margin is likely to increase in the band of 50-100 basis points at constant currency.

Analysts seem quite optimistic about the company. The Zacks Consensus Estimate for fiscal 2025 sales and earnings per share (EPS) is currently pegged at $6.8 billion and $11.08, respectively. These estimates indicate corresponding growth of 2.2% and 7.5% year over year. The consensus estimate for fiscal 2026 sales and EPS is presently $7.1 billion and $12.46, respectively, indicating increases of 4.3% and 12.5%.

Buoyed by such strengths, shares of this apparel and accessories designer have surged 56.7% against the industry’s 5% decline in a year. Given the aforementioned factors, this Zacks Rank #3 (Hold) company seems to be a decent investment bet now.

Key Picks

Some better-ranked companies are G-III Apparel Group GIII, Royal Caribbean RCL and lululemon athletica LULU.

G-III Apparel Group sports a Zacks Rank #1 (Strong Buy), at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

G-III Apparel Group has a trailing four-quarter earnings surprise of 571.8%, on average. The Zacks Consensus Estimate for GIII’s fiscal 2024 sales indicates an increase of 3.3% from the year-ago period’s reported level.

Royal Caribbean sports a Zacks Rank of 1, at present. RCL has a trailing four-quarter earnings surprise of 18.3%, on average.

The consensus estimate for RCL’s 2024 sales and EPS indicates increases of 16.8% and 63.8%, respectively, from the year-ago period’s reported levels.

lululemon athletica is a yoga-inspired athletic apparel company. LULU carries a Zacks Rank # 2 (Buy), at present.

The Zacks Consensus Estimate for lululemon athletica’s current financial-year sales and EPS indicates growth of 11.4% and 11.8%, respectively, from the year-ago corresponding figures. LULU has a trailing four-quarter earnings surprise of 7.4%, on average.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Royal Caribbean Cruises Ltd. (RCL) : Free Stock Analysis Report

Ralph Lauren Corporation (RL) : Free Stock Analysis Report

lululemon athletica inc. (LULU) : Free Stock Analysis Report

G-III Apparel Group, LTD. (GIII) : Free Stock Analysis Report