Yahoo Finance

Yahoo Finance Here's Why You Should Retain McKesson (MCK) Stock for Now

McKessonCorporation MCK is well poised for growth, backed by strategic collaborations and strength in the Distribution Solutions segment. However, the company’s opioid-related litigation expenses are a potential threat.

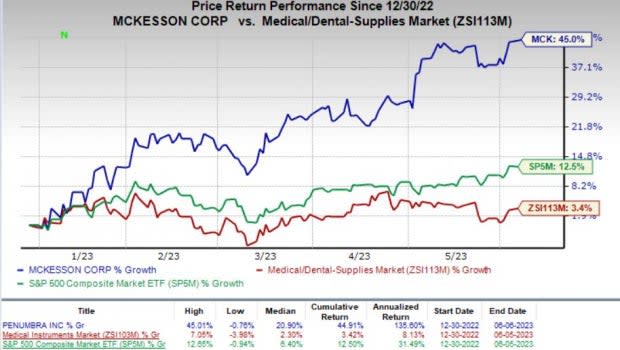

Shares of this Zacks Rank #3 (Hold) company have gained 45% year to date compared with the industry’s 3.4% growth. The S&P 500 Index has risen 12.5% in the same time frame.

McKesson is a healthcare services and information technology company with a market capitalization of $53.6 billion. Its earnings are anticipated to improve 10.8% over the next five years.

The company’s earnings beat estimates in three of the trailing four quarters and missed the same once, the average surprise being 4.48%. Its earnings yield of 6.7% compares favorably with the industry’s 4.8%.

Image Source: Zacks Investment Research

What’s Backing MCK?

McKesson continues to actively pursue deals, divestitures and acquisitions to drive growth. In April 2022, the company completed the divestiture of its retail and distribution businesses in the United Kingdom to Aurelius.

During fiscal 2022, MCK completed the sale of its Austrian business to Quadrifolia management and the remaining share of its German joint venture to Walgreens Boots Alliance.

Earlier this year, the company completed the divestiture of all of its European businesses. These divestitures will allow McKesson to focus on its key growth market — the United States.

In June 2022, MCK formed a joint venture with HCA Healthcare HCA to create a fully integrated oncology research organization. Per the deal, McKesson and HCA will integrate their respective research units — U.S. Oncology Research (USOR) and Sarah Cannon Research Institute (SCRI).

The newly created entity, with the combined capabilities of SCRI and USOR, is expected to boost clinical research, ramp up drug development, lead to better data and analytic capabilities, and pave the way for a wider portfolio of clinical trials. The abovementioned deal was completed in October.

McKesson is a major player in the pharmaceutical and medical supplies distribution market. It stands to benefit from an increased generic utilization and inflation in generics, courtesy of an aging population and several patent expirations in the next few years.The Distribution Solutions segment caters to a wide range of customers and businesses.

During the fiscal fourth quarter of 2023, McKesson’s growth was led by strong performance across all segments, except the International segment, which was marred by unfavorable currency movement. The divestiture of the company’s European business also hurt its growth.

MCK removed a major overhang during the fiscal first quarter by signing a settlement deal related to the opioid-related claims of all 50 states, the District of Columbia and all eligible territories. These developments will close the long-pending litigations that have been hurting the company’s goodwill, as well as reduce the legal expenses.

What’s Hurting the Stock?

McKesson’s broad settlement of opioid-related claims of states and municipalities is likely to drive its short-term expenses. Per the settlement deal, the company had to pay up to approximately $7.4 billion to the Settling Governmental Entities.

Estimates Trend

The Zacks Consensus Estimate for fiscal 2023 revenues is pegged at $275.73 billion, indicating a 4.5% increase from the previous year’s level. The same for adjusted earnings per share (EPS) is pinned at $25.93, implying a 9.5% improvement from the 2022 figure.

McKesson Corporation Price

McKesson Corporation price | McKesson Corporation Quote

Stocks to Consider

A couple of better-ranked stocks from the broader medical space are Merit Medical Systems MMSI and West Pharmaceutical Services WST, each carrying a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Merit Medical Systems has an estimated long-term growth rate of 11%. The company’s earnings surpassed estimates in each of the trailing four quarters, the average surprise being 20.22%.

So far this year, MMSI’s shares have risen 18.9% compared with the industry’s 13.3% growth.

West Pharmaceutical Services has an estimated long-term growth rate of 6.3%. Its earnings surpassed estimates in three of the trailing four quarters and missed the same once, the average surprise being 13.61%.

So far this year, WST’s shares have rallied 49.1% compared with the industry’s 13.3% growth.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

McKesson Corporation (MCK) : Free Stock Analysis Report

Merit Medical Systems, Inc. (MMSI) : Free Stock Analysis Report

HCA Healthcare, Inc. (HCA) : Free Stock Analysis Report

West Pharmaceutical Services, Inc. (WST) : Free Stock Analysis Report