Yahoo Finance

Yahoo Finance Here's Why Investors Should Steer Clear of Norwegian Cruise

Norwegian Cruise Line Holdings Ltd. NCLH has been bearing the brunt of increased expenses, which have been detrimental to its margins. Additionally, high debt burden and the recent travel ban to Cuba are likely to affect the company’s results in the upcoming quarter.

Resultantly, Norwegian Cruise trimmed its outlook for 2019. The company expects adjusted earnings per share to be $5.00-$5.10, down from the earlier $5.40-$5.50. The Zacks Consensus Estimate for its earnings in 2019 stands at $5.08, above the mid-point of the company’s guided range.

Net yield is expected to be 2.6%, lower than Norwegian Cruise’s prior guidance of 4.5%. Meanwhile adjusted net cruise costs are anticipated to be roughly 4.5% in constant currency, higher than previously mentioned 3.5%.

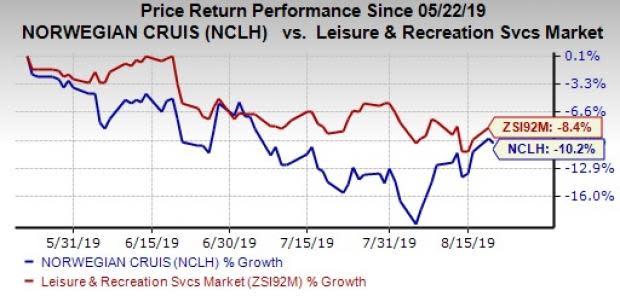

Over the past three months, Norwegian Cruise’s shares have declined 10.2% compared with the industry’s fall of 8.4%.

Let us find out why the Zacks Rank #4 (Sell) company is not a suitable choice for investors at the moment.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

High Expenses & Debt Hurt

Norwegian Cruise is suffering from high expenses for quite some time. Fuel costs and net cruise costs are rising persistently. Moreover, by strengthening the international distribution system, the company may improve yields but at the cost of higher expenses.

In the second quarter of 2019, total cruise operating expenses rose 11.1% year over year. Gross cruise costs per capacity day grew 8.3%. Adjusted Net cruise costs (excluding fuel) per Capacity Day rose 6.1% on a constant-currency basis and 5.1% on a reported basis. Fuel price per metric ton (net of hedges) grew 2.5% to $493 in the quarter.

The company’s heavy reliance on debt financing is concerning. As of Jun 30, 2019, cash and cash equivalents totaled $419.9 million. Long-term debt at the end of the second quarter totaled $5.7 billion. This is further indicated by the fact that the ratio of the company’s long-term debt to capitalization (expressed as a percentage) is currently 48.3. This compares unfavorably with 32.1% for the industry.

Due to higher debt burden, the company might fail to finance upcoming projects. Moreover, any downturn in macroeconomic and credit market conditions would make it difficult for Norwegian Cruise to pay or refinance debt moving ahead.

Intense Competition

The company faces intense competition from other established cruise companies as well as alternative leisure providers. Royal Caribbean RCL and Carnival CCL account for 25% and 44% of global industry capacity, respectively. Meanwhile Norwegian Cruise only accounts for 9% of the global industry. Also, non-cruise-based vacation providers like Marriott Vacations VAC and other tour companies pose substantial threat to Norwegian Cruise’s operations.

Macroeconomic Headwinds

Norwegian Cruise is heavily investing in China, where a slowdown in the economy could limit discretionary spending. In fact, the rate of capacity growth in the Asia Pacific region is expected to slow considerably in the near term for the company and the industry. Further, in Europe, economic/political conditions are expected to be somewhat challenging after the U.K.’s exit from the 28-member economic bloc.

Also, the company generates a significant amount of revenues from customers outside the United States, where the majority pay with local currency. Hence, it is highly exposed to the impact of negative currency translation. Thus, if the U.S. dollar continues to strengthen versus the company’s basket of currencies, it is likely to prove detrimental to its earnings growth. Moreover, an increase in fuel prices may further hamper Norwegian Cruise’s performance.

Meanwhile, Trump administration's policy change on travel to Cuba is concerning. Travel ban to Cuba will have a huge impact on cruise industry at the beginning of summer vacation season as demand for sailings in the region is very high. It will likely impact Norwegian Cruise’s earnings by 35-45 cents in 2019.

Biggest Tech Breakthrough in a Generation

Be among the early investors in the new type of device that experts say could impact society as much as the discovery of electricity. Current technology will soon be outdated and replaced by these new devices. In the process, it’s expected to create 22 million jobs and generate $12.3 trillion in activity.

A select few stocks could skyrocket the most as rollout accelerates for this new tech. Early investors could see gains similar to buying Microsoft in the 1990s. Zacks’ just-released special report reveals 7 stocks to watch. The report is only available for a limited time.

See 7 breakthrough stocks now>>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Marriot Vacations Worldwide Corporation (VAC) : Free Stock Analysis Report

Royal Caribbean Cruises Ltd. (RCL) : Free Stock Analysis Report

Norwegian Cruise Line Holdings Ltd. (NCLH) : Free Stock Analysis Report

Carnival Corporation (CCL) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research