Yahoo Finance

Yahoo Finance Giyani Announces the Results of its Feasibility Study for the K.Hill Battery-Grade Manganese Project

Post-tax NPV at 8% of US$481M, IRR of 28%

Figure 1

Figure 1

Figure 2

Figure 3

Figure 4

Figure 5

Figure 6

Figure 7

Figure 8

Figure 9

Figure 10

Figure 11

Not for distribution to U.S. newswire services or for dissemination in the United States.

TORONTO, Nov. 14, 2022 (GLOBE NEWSWIRE) -- Giyani Metals Corp. (TSXV: EMM, GR: A2DUU8) ("Giyani" or the "Company") is pleased to provide results of the feasibility study ("FS") for the K.Hill battery-grade manganese project in Botswana (the “Project” or “K.Hill”).

The FS has been prepared by SRK Consulting (“SRK”), as lead, on an integrated mining and processing operation for the onsite production of high-purity manganese sulphate monohydrate (“HPMSM”) directly from manganese oxide ore mined at K.Hill. HPMSM is a refined precursor material used in the production of cathode powders for lithium-ion batteries (“LI Batteries”) deployed in electric vehicles (“EVs”).

K.Hill’s total Indicated Resource of 2.1 million tonnes (“Mt”), estimated by SRK in February 2022, was evaluated for the purpose of the FS and almost 100% of the Indicated Resources have been converted into 2.0 Mt of Probable Reserves. The Inferred Resource of 3.1 Mt for K.Hill, estimated by SRK, is in the process of evaluation to be upgraded into the Indicated Resource category. New Mineral Resource Estimates for K.Hill and the nearby Otse manganese oxide prospect are currently targeted for completion in H1 2023.

Highlights¹:

Robust economic returns: a post-tax net present value (“NPV”), at an 8% discount rate, of US$481M (C$649M) and a post-tax internal rate of return (“IRR”) of 28%.

Low capital intensity for what will be one of the largest HPMSM projects in the world: estimated initial capital expenditure of US$281M (C$379M), including contingency of US$32M (C$43M), for a fully integrated battery raw materials project.

Strong free cash flow: net free cash flow over the life of the Project is estimated at US$1,093M (C$1,476M), equivalent to US$99M (C$134M) per year with first commercial production in 2025.

Significant geological upside offers potential to expand Project and extend mine life: exploration work to upgrade the 3.1 Mt of Inferred Resources in the K.Hill southerly extension is progressing and the addition of these resources and the Otse prospect provides the potential to expand the Project in future years and extend the mine life significantly.

Operational advantage of higher grade ore and conventional mining: Giyani's Probable Reserve grade of 18.9% manganese oxide (“MnO”) is the highest among its listed battery-grade manganese peers and underpins a scalable operation with an initial throughput of 200 thousand tonnes (“kt”) ore production per annum, offering potential future production capacity expansion.

LI Battery demand expected to increase significantly: CPM Group LLC (“CPM”), an independent research and consultancy company, projects demand for HPMSM in LI Batteries to grow by nearly 30 times between 2021 and 2036.

Pathway to becoming a low-carbon producer: Giyani’s HPMSM production process directly from manganese oxide ore does not require power-intensive calcining or electrorefining and the planned integration of 4.5 MW of solar power contributes to a very competitive Scope 1 and 2 emissions footprint of only 1.4 kg of carbon dioxide equivalent per kilogram of HPMSM (see Giyani News Release of September 29, 2022).

Strong environmental, social and governance (“ESG”) credentials: the Project’s development strategy has been formulated around the mitigation hierarchy of “avoid-minimize-mitigate” with initiatives such as renewable energy integration, water self-sufficiency and dry stack tailings management to be included in the Environmental and Social Impact Assessment (“ESIA”), currently estimated to be completed and submitted to the authorities in Botswana in Q1 2023.

Optimization work opens opportunities for enhancing Project value: in addition to potential life-of-project (“LOP”) extensions through further exploration success, work is ongoing to lower operating costs, particularly related to certain consumables affected by supply chain disruption and global inflation.

Jonathan Henry, Executive Chair of Giyani, commented:

Our flagship K.Hill manganese project has the potential to be one of the most significant and largest battery-grade manganese producers globally. The feasibility study shows how far the scope of the Project has developed since the April 2021 preliminary economic assessment and is the next step to bringing this project into production. These results demonstrate the robust economics of K.Hill, with our ongoing work also highlighting the expansion and optimization potential.

Giyani has an early-mover advantage to meet the growing demand for HPMSM from the EV sector, which is prioritizing responsible, low-carbon producers outside of the dominant Chinese supply chain. Our hydrometallurgical process, which treats our captive ore without the need for calcining or electrorefining, saves both cost and carbon emissions, as evidenced by the results of the recent life cycle assessment for K.Hill.

Alongside the optimization work that will be completed after the FS release, which will review opportunities to enhance the Project’s value, we continue to evaluate the 3.1 Mt of Inferred Resources at K.Hill and potential additional resources at nearby Otse still to be consolidated into the Project plan, with the view to extend K.Hill’s operating life and production capacity significantly.

In parallel to the FS work, the team has progressed the construction of our demonstration plant and it remains on track to produce HPMSM samples for testing by potential off-takers in H2 2023.

Operational and Economic Highlights

The FS is based on a Probable Reserve Estimate that will be detailed in the updated National Instrument ("NI") 43-101 Technical Report on the Project. The NI 43-101 report will include results of the FS and be filed within 45 days of this release on SEDAR at www.sedar.com and made available on the Company’s website at www.giyanimetals.com. All financial figures are quoted in US dollars unless otherwise stated and the numbers in the tables below may not add exactly due to rounding.

Table 1 Project overview

Metrics | Units | Results | |

Project summary | |||

Type of mine | ‑ | Conventional open pit mine | |

Type of production facility | ‑ | HPMSM hydrometallurgical processing | |

Life of the Project (“LOP”) | years | 11.0 | |

Net realized price assumption | |||

Average realized HPMSM price (Yr 1 – 5) | $/t | 3,373 | |

Flat realized price HPMSM price (Yr 6 – 11) | $/t | 3,918 | |

Production | Annual | LOP | |

Total ore mined | dry kt | 226 | 2,032 |

Run-of-mine (“RoM”) manganese oxide grade | % MnO | 18.9 | 18.9 |

Steady-state metallurgical recovery | % | 88.5% | 88.5% |

Total recovered manganese oxide | kt MnO | 31 | 339 |

Total HPMSM produced | kt | 73 | 808 |

Project cash flow | Average annual | LOP | |

Revenue from HPMSM | $M | 272 | 2,993 |

Total operating costs (incl. royalty) | $M | 125 | 1,369 |

Total EBITDA | $M | 148 | 1,624 |

Initial capital expenditure excl. contingency | $M | ‑ | 249 |

Contingency on initial capital | $M | - | 32 |

Total initial capital expenditure incl. contingency | $M | - | 281 |

Sustaining capital expenditure incl. contingency | $M | - | 21 |

Closure costs | $M | ‑ | 5 |

Total LOP capital expenditure incl. contingency | $M | ‑ | 307 |

Project economics | Pre-tax | Post-tax | |

NPV (8% real discount rate) | $M | 603 | 481 |

IRR | % | 32.0 | 28.3 |

Payback period from start of processing | years | 3.3 | 3.6 |

Cumulative cash flow, undiscounted | $M | 1,317 | 1,093 |

Notes: | |||

Economic Analysis

A technical economic model (“TEM”), prepared by SRK on a 100% equity basis, demonstrates that K.Hill provides a robust post-tax NPV at an 8% discount rate of US$481M (C$649M) and a post-tax IRR of 28% in real terms. The TEM uses HPMSM forecast prices provided by CPM for the Company’s key markets of Europe and North America, but adjusted to run a flat price from Year 6 of the production period.

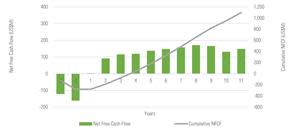

Free cash flow over the LOP is estimated at US$1,093M (C$1,476M), equivalent to US$99M (C$137M) per year (Figure 1). Payback of initial capital expenditure is estimated to be approximately 3.6 years from start of production (Table 2).

Figure 1 is available at

https://www.globenewswire.com/NewsRoom/AttachmentNg/61babfb4-c4d4-4d53-9221-268b26622ac1

https://www.globenewswire.com/NewsRoom/AttachmentNg/fa1dfa8e-10b3-490b-bdeb-74fddc3700d5

Table 2 Valuation metrics

Metric | Unit | Pre-tax | Post-tax |

NPV 5% | $M | 808 | 656 |

NPV 8% | $M | 603 | 481 |

NPV 10% | $M | 495 | 388 |

Payback period, from start of processing | Years | 3.3 | 3.6 |

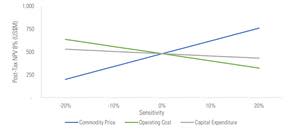

A sensitivity analysis was run on the key variables affecting Project economics and NPV. The results of the sensitivity analysis are shown in Figure 2 below and include the assumed flat pricing structure from Year 6 outlined above.

Figure 2 is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/06e3fef5-bf3b-4d1e-b1df-38dedb25b724

Taxation

For the purposes of the TEM, following a review of the Botswana tax regime and discussions with local stakeholders, it has been assumed that the Project will be subdivided into two business units with discrete tax treatment: mining; and manufacturing.

The mining operation will sell ore to the manufacturing operation and be taxed according to the Botswana mining company tax formula (minimum of 22% on operating income). A mining royalty of 3% will be applied to the revenue on the sale of the manganese ore to the manufacturing unit. Capital investments on the mining unit can be depreciated in the year incurred and unredeemed capital will be carried forward indefinitely.

Income from the manufacturing unit will be taxed at the Botswana manufacturing tax rate of 15%, assuming a manufacturing development order will be received from the Botswana authorities. For the manufacturing unit, initial capital investments will depreciate at 10% per year on a straight-line basis and sustaining capital will depreciate at 20% per year.

Capital and Operating Expenditures

Capital and operating expenditure estimates were provided by SRK and Coffey Geotechnics Ltd., a Tetra Tech Inc. company (“Tetra Tech”).

Capital expenditure

Capital expenditure estimates were prepared for initial, sustaining and closure capital.

The total estimated initial capital expenditure for the design, construction, installation, and commissioning for all facilities and equipment for the Project is US$281M including contingency of US$32M. This estimate includes direct field costs required to execute the Project, plus indirect costs associated with design, construction, installation, and commissioning. This estimate is based on pricing as of H2 2022, with no allowances for inflation or escalation (Table 3). Closure costs of US$5M have been estimated.

This estimate is a Class 3 estimate prepared in accordance with the Association for the Advancement of Cost Engineering (AACE®) International Cost Estimate Classification System. The accuracy of the estimate is ‑10% to +15%.

Table 3 Summary of LOP capital expenditures

Area | Total (US$M) |

Mining | 10.5 |

Processing | 98.1 |

Infrastructure and services | 31.2 |

Tailings management facility (“TMF”) | 6.6 |

Offsite infrastructure | 9.7 |

Indirect costs (including first fill and commissioning costs) | 65.5 |

Construction overheads | 21.6 |

Owner’s costs | 5.5 |

Total initial capital expenditure excluding contingency | 248.7 |

Contingency on initial capital expenditure | 32.0 |

Total initial capital expenditure including contingency | 280.7 |

Sustaining capital including contingency | 21.4 |

Closure cost | 5.1 |

Total | 307.3 |

Contingencies on initial capital expenditure have been added at appropriate percentages to each area resulting in a contingency of US$32M or 13% of direct and indirect expenditure in relation to the initial capital expenditure.

Capital expenditures incurred after start-up are assigned to sustaining capital and are projected to be paid out of operating cash flows. In keeping with industry practice, the annual sustaining capital allowance has been estimated as 2.5% of the hydrometallurgical plant direct capital cost over a period of 8 years totalling US$21M (including 15% contingency of US$3M). Figure 3 shows the breakdown of the initial Project capital expenditure by area.

Figure 3 is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/f97d7e91-f52a-4525-a02c-28d8b23cd26f

Operating expenditure

Operating expenditure has been derived for:

open pit mining (inclusive of water management) and labour;

mineral processing;

tailings management; and

general & administrative (“G&A”).

Total operating expenditure for K.Hill is expected to average around US$672/t milled based on an average annual RoM throughput of 200 kt/a, excluding royalties, as shown in Table 4 below. Processing expenditure accounts for around 95% of the total operating expenditure of the Project.

Table 4 Summary of Project operating expenditure per tonne processed

Area | Operating cost |

Mining | 20.0 |

Processing | 636.4 |

Tailings management | 2.0 |

G&A | 13.4 |

Total operating costs | 671.8 |

Notes: | |

Metallurgical processing reagents and raw materials constitute the largest component of processing expenditure based on the plant design criteria and flowsheet to produce HPMSM.

Figure 4 shows that the processing reagent expenditure accounts for approximately 73% (US$92M annually) of the direct expenditure. However, of the total reagent expenditure, approximately 36% is associated with importation and freight costs of certain key reagents currently assumed to be sourced on the international markets.

Figure 4 is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/5f9b2f8b-048f-490d-bd62-b38bb594e410

During 2021 and early 2022, Covid-19 related disruptions led to an unprecedented rise in international freight rates, which elevated prices for the procurement of reagents. Since mid-2022, international freight rates have seen declines of between 50 – 75%² and are expected to continue to normalize towards pre-Covid levels.

As part of its post-FS activities, detailed below, Giyani has commenced the process of identifying opportunities to reduce operating expenditure by lowering consumption of certain key reagents and developing local or alternative sources of reagents to mitigate international freight costs.

Working capital

An allowance for working capital is included in the TEM and reflected in the cash flow with the following delays assumed:

Debtors: 90 days;

Creditors: 60 days; and

Stores: 30 – 60 days.

Commissioning and ramp-up

The TEM assumes plant commissioning over two quarters followed by an S-curve ramp-up schedule to reflect the sophisticated nature of the K.Hill processing plant. Ramp-up has been staged over a conservative eight-quarter period and metallurgical recoveries are assumed to start at 75.0% and rise to 88.5% by completion.

HPMSM Pricing

CPM, an independent research and consultancy company based in New York and specialist in analysis of the high-purity manganese market, completed a HPMSM products market outlook study for the FS.

The study projects demand for LI Batteries used in EVs to grow by 25% annually between 2021 and 2031 and that demand for HPMSM in LI Batteries will grow nearly 30 times between 2021 and 2036, reaching 1.8 Mt on a contained metal basis, and may reach 4.5 Mt by 2050.

Utilization of high-purity manganese by the LI Battery sector is forecast to increase in the coming years as end-users seek to reduce cobalt use in nickel-manganese-cobalt (“NMC”) cathode formulations and increase manganese use in iron in lithium-iron-phosphate (“LFP”) cathode formulations. In 2018, the German chemical giant BASF announced new NMC 370 and NMC 271 cathodes with an expected cobalt content of less than 5% and significantly increased manganese content of 75% or more. Several companies are also working on different variations of the manganese-bearing LFP chemistry, where the addition of manganese could potentially improve energy density by up to 20%, while reducing the material cost by up to 28%.

Based on forecasts from CPM and E Source Companies LLC (“E Source") for EV production and LI Battery cathode chemistries, total demand for HPMSM is expected to surpass 1.6 Mt/a by 2035, on a contained metal basis. With current global HPMSM production capacity of approximately 0.1 Mt/a (contained metal) and total global production, including the known pipeline of new projects, expected to reach only 0.8 Mt/a by 2035, consumers are facing a projected supply deficit of 0.8 Mtpa by the middle of the next decade.

Currently, only six non-Chinese high-purity manganese projects are forecast to come on stream in the next five years, producing only 0.1 Mt/a (contained metal). China may be the source of an additional 0.2 Mt/a by 2027, but there are doubts as to the purity of this material due to the use of selenium containing manganese metal as a feedstock, which would likely be unsaleable in European or North American markets.

The chart in Figure 5 illustrates a 10-year projection of the forecast supply-demand balance for HPMSM to 2035 and Giyani’s estimated share of the global market. CPM has assumed a 50% recycling rate from used LI Batteries, although it considers this to be unlikely given that no manganese is currently recovered in the recycling process because of its low economic value.

Figure 5 is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/45512fd4-04c3-4e3b-b2a8-1e8cef7beb92

Note: figures above are quoted in tonnes of HPMSM, not metal contained.

Source: E Source, International Manganese Institute, industry sources, CPM

The contractual prices between sellers and buyers of HPMSM are largely detached from the prices of other manganese products. Manganese is also the cheapest of all battery metals and, despite having an equal weight to cobalt, it accounts for only 1% to 2% of the cost of the cathode materials depending on the applicable cathode chemistry. This makes manganese prices insensitive for cathode makers.

Net HPMSM prices realized at the Project’s gate used in the TEM assume 50% of sales to the EU (Berlin) and 50% sales to North America (Detroit). CPM provided pricing forecasts for HPMSM in both EU and North American markets to 2035, however, in consultation with the Company, for the purposes of the TEM and valuation, SRK adopted a flat composite price of US$3,918/t HPMSM from Year 6 (2030) of the Project’s commencement of production to end of the LOP.

Table 5 Average net realized HPMSM prices used by SRK and forecast by CPM

Calendar Year | Used by SRK | CPM Forecast Price |

2026 | 2,993 | 2,993 |

2027 | 3,250 | 3,250 |

2028 | 3,517 | 3,517 |

2029 | 3,775 | 3,775 |

2030 | 3,918 | 3,918 |

2031 | 3,918 | 4,147 |

2032 | 3,918 | 4,427 |

2033 | 3,918 | 4,729 |

2034 | 3,918 | 5,053 |

2035 | 3,918 | 5,499 |

LOP Average | 3,704 | 4,131 |

Notes: | ||

Mineral Reserve Statement

In October 2022, SRK estimated Mineral Reserves for the Project of 2,032 kt of ore with 18.9% MnO at a cut-off grade of 7.3% MnO. Modifying factors for dilution and recovery have been applied at the rate of 3% dilution and 98% recovery applied on the Mineral Resource block model.

Mineral Reserves have been estimated in accordance with the CIM Estimation of Mineral Resources & Mineral Reserves Best Practice Guidelines (CIM 2019) and classified according to the definitions presented in CIM Definition Standards for Mineral Resources & Mineral Reserves (CIM 2014). The QP is Mr. Michael Beare, B.Eng, CEng, ACSM, MIMMM, who visited the site between December 16 – 18, 2019.

Table 6 Mineral Reserve estimate for the K.Hill Project as of October, 2022

Classification | Tonnes | MnO Grade | MnO Contained Metal |

Probable Reserve | 2,032 | 18.9 | 384 |

The Mineral Reserve for the Project is a subset of the Indicated Resource. SRK completed an updated Mineral Resource estimate for K.Hill in February 2022 as announced by the Company on February 16, 2022. Considering the absence of Measured Resources, Probable Mineral Reserves have been modified from Indicated Resources only. Inferred Resources have been set as waste.

Mining

The K.Hill orebody will be extracted in an open pit using a conventional truck-and-shovel mining method. The TEM assumes owner operated mining methods and equipment. The orebody will be mined in a three-zone cutback sequence, starting on the upper section of the southern flank of the pit. Material mined will be sent to either the plant, the stockpile, or the waste rock dump (“WRD”). The pit design parameters are supported by the geotechnical assessment implementing a 41° overall slope, including 4 m bench heights that are planned to be mined out in 2 m flitches. Backhoe excavators equipped with 4 m3 buckets will load selectively into 30 t haul trucks.

Figure 6 is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/98639650-1efb-4def-b2ab-f3232937a70c

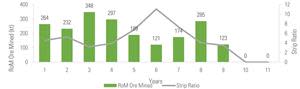

The K.Hill final pit design contains 2,032 kt of ore at 18.9% MnO above a cutoff of 7.3% MnO (excluding 3.1 Mt of Inferred material in the southerly extension of the deposit and outside the FS pit shell). The mine plan includes 8.5 years of mining with an additional 2.5 years of stockpile rehandling and processing, which results in a total operational LOP of approximately 11 years. Any of the additional 3.1 Mt of Inferred Resources, which lie to the south of the FS Probable Reserve and may in future be upgraded to Indicated category, would be expected to extend the LOP. Evaluation work on this southerly extension of the K.Hill deposit is ongoing, with infill drilling having been completed earlier in 2022.

The WRDs are planned to be constructed to the east of the proposed pit, with a total capacity of 11.4 Mt. The WRDs overall slopes have been designed at 20°, which is appropriate for immediate dump rehabilitation as part of progressive mine closure. A RoM stockpile with a peak quantity of 350 kt is planned to be built 50 m north of the process plant, allowing for easy rehandling to the RoM pad.

Geotechnical data shows that 45% of the K.Hill material has been classified as hard digging and 12% classified as very hard digging. The remainder of the material is classified as free, easy or medium digging. A crawler tractor will rip most of the material to assist the excavator in maintaining the production rate. Owing to the likely variance in material strength, small-scale blasting will be undertaken. This will allow for a smooth ongoing operation with minimum downtimes and reduce wear on machine tools when very hard material is encountered.

Processing

Tetra Tech recommended and supervised a complete feasibility-level metallurgical test work program at Mintek, a mineral processing, metallurgical laboratory and research facility based in Johannesburg, South Africa. Specialist laboratory and consulting engineers completed supplementary test work in dewatering and crystallization, respectively. Apart from the standard crushing and grinding test work, additional test work was designed to characterize the leach and selective precipitation behaviour of a representative ore sample.

The test work program successfully validated the flowsheet and produced, from a K.Hill ore sample, HPMSM crystals that meet the requirements of international buyers (Figure 7). Laboratory and crystallisation test work has demonstrated that HPMSM of not less than 99.97% purity can be produced. The overall manganese recovery was demonstrated to be up to 88.5%. Certain potential future off-takers have requested samples of HPMSM crystals produced during test work.

Figure 7 is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/225036af-f846-44d0-9379-b344bf852f20

The process plant will treat 200 kt/a of RoM ore from the open pit, and the plant will have a nameplate production capacity of up to 120 kt/a HPMSM crystals, depending on ore characteristics. First, the ore will be crushed and milled to a characteristic grind (P80) of 150 µm. The resulting slurry, comprising mainly manganese and iron shales, is moderately hard and amenable to reductive acid leaching in sulphate media using sulphur dioxide as a reductant. Sequential precipitation and solid/liquid separation steps will systematically remove metal impurities from the leachate to produce a purified solution. Trace contaminants will be removed using fluoride polishing. From this stock solution, the HPMSM will be crystallized in an energy efficient, bespoke designed mechanical vapour recompression crystallizer. The crystallizer will incorporate an integrated three-stage evaporative crystallizer and dewatering circuit. The final product will be a dried HPMSM crystalline product packaged for transport in sealed bulk bags.

The envisaged annual rate of production of 200 kt/a through the processing plant will be achieved on a continuous basis after commissioning and a two-year ramp-up, through a combination of direct ore feeding and stockpile rehandling. This will continue until full depletion in Year 11. Production will peak at 89 kt/a HPMSM with an LOP average of approximately 73 kt/a HPMSM at an average ore grade of 18.9% MnO.

Figure 8 is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/c2de630d-5797-41f6-9043-3d05170fb05c

Non-hazardous waste material from the process will be disposed in the TMF as a filter cake. Base metal sulphides will be stored as an intermediate product and will be sold to smelters in South Africa or disposed of at an appropriate facility. Any sales receipts or possible disposal costs have not been included in the TEM and would be insignificant in quantum. All liquors removed in the treatment of the ore will be treated for either reuse or, if non-hazardous, used for haul road dust suppression.

Tailings Management Facility

Various standards were referenced for the design of the TMF (e.g., Global Industry Standard on Tailings Management (August 2020); Canadian Dam Association Application of Dam Safety Guidelines to Mining Dams (CDA 2014)).

The TMF will be a zero-discharge dry stack facility located southeast of the process plant. It will comprise a fully lined filtered storage area and clarification pond to collect runoff and any seepage water. Tailings material will form filter cakes from solid-liquid separation stages using pressure filtration combined with a small amount of water treatment effluent. The water from the clarification pond will be returned to the process plant via a return line and pump.

Tailings will be delivered to the storage site using a single 30 t articulated dump truck similar to the ones used by the mining fleet. Tailings will be loaded from the stockpile outside the process plant onto the truck. Upon deposition at the TMF site, tailings will be spread and nominally compacted by a dozer. After the material has been spread, an 11 t (or heavier) sheepsfoot roller will be used to compress the material to a degree of compaction of at least 92% standard Proctor maximum dry density.

As the moisture content after compaction will also be relatively high, it is not expected that dust will be generated on the surface before the next layer is placed. During construction no dust-related problems are foreseen; however, for the closure of the structure, some dust control measures will likely be necessary.

The TMF will be closed progressively by covering the surface with vegetation to minimize water ingress and erosion of faces while decreasing the potential for dust generation. Due to the absence of ponded water, tailings dewatering has been considered unlikely, as it is assumed the stack will be free draining. The closure plan is designed to be a “walk away” solution subject to a full Closure Management Plan and taking into account appropriate redeployment of infrastructure, alternative employment and retrenchment. Diversion channels north of the TMF will divert surface water runoff.

Project Infrastructure

Regional access

The K.Hill site is accessible via a network of paved national and local roads. The A2 highway that runs from Buitepos at the Namibian border, through Jwaneng, Kanye and Lobatse in Botswana, to the South African border at Pioneer Gate near Zeerust, passes within 5 km of the Project site. The A2 highway forms a major component of the Trans-Kalahari Corridor, which is a highway corridor that provides a direct route from Maputo, Mozambique, through Pretoria, South Africa, to Windhoek in central Namibia, and ends at the port of Walvis Bay in Namibia.

The main access road to the mine site will run from Kanye via the Mmathethe gravel road, which will be upgraded to meet the requirements for transporting materials and personnel to and from the site. The road design will comply with general practice in highway engineering, including minimum slope inclines, properly banked curves, minimum sight distance, and horizontal and vertical alignment to ensure safe and efficient roads for quick and economical movement to the site.

Site layout

As per guidelines from the Botswana Department of Mines, the boundary of the Project footprint is sufficient for the mine and associated infrastructure but is not excessive for the mine requirements.

Figure 9 is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/636b4eab-6346-4d38-9a51-35891a759aa5

Vehicular access to the site will be controlled to provide security for personnel and property and to manage the risk to the mining and processing operations. The gatehouse will consist of a four-bay truck parking area, a guard house, two weighbridges, and control room and site gate. An administration block to the west of the process plant will provide office and change facilities. The fuel storage facility with a capacity of 75,000 litres of diesel will be located on a bunded concrete pad (Figure 10).

The layout of the process plant has been designed with sufficient space to accommodate potential plant expansion in the likely event that additional resources justify a future increase in Project throughput and production capacity.

Figure 10 is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/e07d32e2-45c8-443f-a9d4-1f1e353d4670

A light steel industrial warehouse with a fenced laydown area will be used to store spares and minor consumables. The maintenance strategy is to complete simple, routine, and minor maintenance on site. Major overhaul and fabrication will be completed offsite in Kanye, Gaborone, or in South Africa. The site will include a mechanical/electrical workshop as well as a truck shop. Another warehouse adjacent to the crystallizer will house both the bagging plant and securely store the final product.

Figure 11 is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/0b41fe88-0433-4ac2-8762-28228fe533f1

Water

Analysis and mapping of the available groundwater level data indicates that the pit floor will remain above the water table throughout the life of the Project.

There are no perennial watercourses within the Project site; therefore, surface water management focuses on stormwater management. Surface water draining into the open pit is estimated to be 4,000 m3/day during storm events at a frequency of once every two years. Water that accumulates within the pit will be used for dust suppression or treated for use in the process plant.

WRD runoff will follow the site topography and drain to the southeast in the form of surface water runoff and lateral seepage. The drained water will be intercepted by collection channels along the southern and eastern boundaries of the WRD. This water will be channelled to the low topographic points south and east of the WRD where a sedimentation pond in each location is proposed to control settling of suspended solids and water quality. This water will be transferred to the TMF clarification pond.

Apart from a sump in the open pit, the largest water storage capacity on the site will be the TMF clarification pond, which will also act as a stormwater pond. Water from this pond will be recycled to the process plant to offset raw water makeup and maintain maximum live capacity. Although not anticipated to be an issue, return water will need to be tested to prevent the introduction of unanticipated contaminants.

The Water Utilities Corporation (“WUC”), the Botswanan state-owned utility company, will supply raw water from the Kgwakgwe pump station located approximately 0.5 km from the site gate. The water requirement for the Project is 45 m3/h. WUC will supply 20 m3/h, and the balance will come from groundwater from three boreholes Giyani has drilled and owns; pump tests have indicated that more than the required amount could be delivered. In agreement with WUC, Giyani will inject this water into the WUC water supply system near the boreholes and extract the full amount via the Kgwakgwe pump station.

Power

The Botswana Power Corporation (“BPC”) issued a letter dated June 30, 2022, agreeing to provide power supply infrastructure for the Project. A total load demand of around 15 MVA is expected for this development phase, however, BPC will provide for a total load demand of 30 MVA in the form of a 132/33 kV substation, fed via a new 19 km, 132 kV transmission line from the Mmakgodumo substation situated on the northern outskirts of Kanye along the Kanye-Lobatse bypass road. A new 132/11 kV substation will be located within the vicinity of the K.Hill site. The supply will be sized to accommodate a future potential expansion of the production capacity of the Project.

Motor control centre (“MCC”) nodes will be serviced at an 11 kV level through local ring main units. Electrical users have been functionally grouped into MCC nodes according to the process flow diagrams and considering the geographical location of consumers. The MCC nodes will be connected to the 11 kV supply network either as 11 kV loads or as 400 V loads connected though 11 kV/400 V stepdown transformers.

The Company has the objective of being a low-carbon supplier of critical LI Battery raw materials for the EV industry. On September 29, 2022, the Company announced the results of a life cycle assessment prepared by Minviro Limited estimating that the production process detailed in the FS would have a global warming potential (“GWP”) of 3.2 kg carbon dioxide equivalent (“CO2 eq”) per kg HPMSM, of which Scope 1 and Scope 2 emissions amount to 1.4 kg CO2 eq. per kg HPMSM.

The main impact driver of the GWP is the consumption of electricity from the national grid in Botswana, corresponding to approximately 37% of total GWP. Owing to the excellent solar radiation conditions in Botswana, Giyani identified solar power generation as an opportunity to further reduce the Project’s already low carbon footprint. The Project includes a 4.5 MW photovoltaic solar plant, as detailed below, and Giyani is assessing various options to further reduce the GWP for K.Hill and to develop a roadmap for decarbonization.

Solar plant

The 4.5 MW solar plant for the Project will be located on a 7.6 ha area 1.2 km west-northwest of the Kanye municipal borehole. This location was selected to take advantage of the relatively flat topography west of the mine and to position the solar plant outside of an area that would be affected in the unlikely event of any dust plume coming from the mine, for which dominant wind direction and speeds were accounted.

ESIA and permitting

The Project will comply with Botswana legislation and conform with international standards, notably, Equator Principles (EP4) (2020) and the International Finance Corporation Performance Standards on Environmental and Social Sustainability (2012).

The Project is located on tribal land that has been disturbed by small-scale farming, previous mining operations, and construction of infrastructure (water reservoirs and communication tower with concrete access road). Thus, this is a brownfield site. Negotiations with the owners of the infrastructure are advanced and they have agreed to it being relocated. Sites have been identified; therefore, the relocation process will not hinder the Project schedule. During meetings with local Chiefs and environmental consultants, local farmers have indicated that they are willing to move. The Land Board is custodian of the tribal land and will facilitate identifying new areas for the farmers to move to.

The Botswana Department of Environmental Affairs (“DEA”) has given authorization for all exploration activities on K.Hill after reviewing an Environmental Management Plan (“EMP”) submitted by Loci Environmental (Pty) Limited (local consultants based in Gaborone) on behalf of Giyani. The authorization is valid until September 2024 and may be renewed.

An ESIA, with stakeholder engagement, is ongoing in accordance with Section 9(1) of the Botswana Environmental Assessment Act. A scoping report and terms of reference were submitted to, and approved by the DEA, enabling the ESIA to begin. To date, thirteen specialist studies have been drafted to address the biophysical and socio-economic aspects of the environment. In response to the results of trade-off studies and changes to the Project, some of the specialist studies are being revised (e.g., dry stack tailings vs. conventional tailings; changes to processing to reduce energy consumption; and a solar farm to reduce reliance on coal-based grid power). Environmental authorization, based on DEA review of the ESIA, will enable applications to be made for other necessary authorizations and permits (e.g., change of land use and mining licence). To date, no fatal flaws or red flags have been identified.

Project Execution Plan

The FS sets out a realistic project execution plan based on the scope of what will be designed, procured, built, and commissioned. The plan includes a description of activities undertaken leading up to Project execution: the execution scope, strategy, schedule, and compliance with all ESG and health, safety, and environment (“HSE”) guidelines and best practices.

Initial project objectives

The Project will be executed to achieve the following initial project objectives:

Delivery of a process plant that can achieve HPMSM production of approximately 80 kt/a, on average, with the safest standards and in full compliance with all laws and regulations in place at the lowest operating expenditure possible;

compliance with the management and monitoring plans set out in the ESIA, conditions that the DEA will apply to the environmental authorization, and other conditions stipulated in the mining licence;

compliance with HSE management plans, monitoring plans, policies, and procedures; and

on time and on budget Project execution.

Project delivery model

The Project is expected to use an engineering, procurement, and construction management (“EPCM”) project delivery model. The appointed EPCM contractor will be responsible for the majority of the scope, but some work packages may also be undertaken and managed by Giyani’s owner’s team.

Stakeholder engagement

Stakeholder engagement will be managed through a stakeholder engagement plan (“SEP”) that applies to the life of the Project (i.e., from construction to rehabilitation and closure). The SEP will incorporate and build on the consultation associated with the ESIA. Stakeholder engagement will comply with legislative and regulatory requirements and conform with international standards. The SEP will be a live document that will be updated throughout the LOP.

Stakeholders to be engaged through the SEP comprise:

authorities at local, regional, and national levels, including the Departments of Mines, Environmental Affairs, Water and Sanitation, and National Roads; Kanye Administrative Authority, council, Paramount Chief and other Chiefs, Village Development Committees, and Land Boards;

communities and land users: these are mostly directly affected parties including the population of Kanye, local communities, farmers, those using access routes across or adjacent to the Project, and residents and businesses along access routes;

the Project workforce;

national utility companies such as BPC and WUC, and the Botswana Communications Regulatory Authority;

service providers such as the fire department, police, traffic police, emergency response and ambulance as well as hospitals and clinics, both public and private;

suppliers of materials and goods such as fuel, building materials, and reagents; and

off-takers and customers.

Engineering

The engineering design will meet technical, regulatory, and functional requirements. Giyani will undertake a program of value engineering before starting with basic and then detailed engineering.

Long-lead items will be specified for procurement during basic engineering, and general equipment and instrumentation specification will be specified for procurement at the start of detailed engineering. Readily available off-the-shelf equipment will be selected, where possible, taking care to consider maintenance and spare requirements throughout the LOP.

Even though Giyani will seek to use local fabricators, it is anticipated that most of the equipment and bulk materials will be sourced from South African vendors and fabricators or imported via Southern Africa. Plant and infrastructure components will be pre-assembled as much as possible in road transportable units to minimize erection time on site.

Procurement and contracting

Procurement will be managed on behalf of Giyani by the appointed engineering firms, adhering to the principles of thorough pre-qualification, complete life-cycle procurement, and a formal tender process. Shortlisted vendors will have a demonstrated track record and the capacity to deliver and service Southern Africa.

Giyani will distribute the work over several key contracts, selected following a formal tender process. Contractors will be identified and shortlisted as per the pre-qualification process; contracting with a Botswana legal entity will be considered an advantage.

Commissioning

The owner’s team will have a dedicated team to facilitate commissioning and handover to operations. Commissioning will be undertaken by an engineering consultant who specializes in hydrometallurgical systems and who will be integrated into the owner’s team and brought on board during the pre-commissioning execution phase to prepare and finalize the commissioning plan. This team will be responsible for managing the equipment vendor representatives.

Schedule

Key milestone dates for the Project used in the TEM are shown in Table 7. The dates provided below are based on a technical execution schedule under a 100% financed basis and not adjusted for specific commercial and funding assumptions and so do not yet represent a firm timeline for full Project development.

Table 7 K.Hill TEM key milestone dates

TEM Milestone | Date |

Start basic engineering | Q3 2023 |

Start mine pre stripping | Q4 2024 |

Start plant commissioning | Q2 2025 |

First commercial production | Q3 2025 |

End of ramp-up | Q3 2027 |

It should be noted that Environmental and Social Management Plans (“ESMPs”) and Giyani’s policies and procedures will be applied throughout the LOP. Specific ESMPs will be developed before construction begins in readiness for implementation from the outset of construction (e.g., Emergency Preparedness and Response Plan; Water Management Plan; Alien Invasive Species Management Plan).

Post-FS activities

Giyani intends to undertake a series of post-FS activities to optimize aspects of the Project, lower operating costs, develop opportunities and mitigate residual risk. Key immediate workstreams will include the following:

Demonstration plant: the demonstration plant is under construction in South Africa and will be assembled in road transportable modules with a production capacity of up to 600 kg/d of dry HPMSM crystals. The objective is to provide HPMSM samples to potential buyers for their supply chain testing and product qualification and to de-risk the commercial plant development by using the demonstration plant for optimization of the ongoing process engineering work. The demonstration plant is currently expected to be constructed and commissioned by mid-2023 with first samples shipped to potential buyers in H2 2023.

Optimisation test work: Giyani will implement key recommendations from the FS work to optimize the process flowsheet and identify opportunities to reduce operating costs by lowering reagent consumption or developing local sources. This activity includes material characterization to support final equipment selection, such as solid liquid separation and rheology tests. Many of these tests will be completed by vendors or specialist laboratories using intermediate product produced in sufficient quantity by the demonstration plant.

Value engineering: Giyani will undertake a value-engineering program as part of the final optimization of the Project scheme prior to the commencement of basic engineering in anticipation of a final investment decision.

Qualified Persons

The Qualified Person (“QP”) (as that term is defined by NI 43-101) responsible for preparing the FS is Michael John Beare, BEng, CEng, MIOM of SRK. Mr. Beare has reviewed and approved the scientific and technical content contained in this news release and verified the underlying technical data. Mr. Beare is independent of the Company and personal inspections of the Project were made by Mr. Beare between December 16 and 18, 2019.

The QP in accordance with the Canadian Institute of Mining, Metallurgy and Petroleum Code (“CIM Code”), with responsibility for the reporting of the Mineral Reserve Statement presented is Mr. Beare. The QP under NI 43-101 responsibility for the reporting of the Mineral Resource Statement for the Project is Mr. Peter Gleeson, BSc, MSc, CEng, AIGS, MIMMM (CP), a Corporate Consultant (Resource Geology) with SRK. Mr. Gleeson has the relevant experience in reporting Mineral Resources on various base, precious and ferrous metal assets globally. Mr. Gleeson inspected the Project between the January 17 and 21, 2022.

EUR ING Andrew Carter BSc, CEng, MIMMM, MSAIMM, SME Technical Director Coffey Geotechnics Ltd. is a QP under NI 43-101 and is responsible for the metallurgical test work results, process engineering, process operating costs and plant and infrastructure capital cost estimates in this news release.

Neither SRK, Tetra Tech nor the QPs of the FS, has or have had previously, any material interest in Giyani or the mineral properties in which Giyani has an interest. The relationship with Giyani is solely one of professional association between client and independent consultant. The FS is prepared in return for professional fees based upon agreed commercial rates and the payment of these fees is in no way contingent on the results of the FS or the contents of this news release.

About Giyani

Giyani is a mineral resource company focused on becoming one of Africa’s first low-carbon producers of high-purity manganese sulphate precursor materials directly from manganese oxide ore, used by battery manufacturers for the expanding EV market, through the advancement of its manganese assets in the Kanye Basin in south-eastern Botswana, (the “Kanye Basin Prospects”) through its wholly-owned Botswana subsidiary Menzi Battery Metals (Pty) Limited. The Company’s Kanye Basin Prospects consist of eight prospecting licences and include the past producing Kgwakgwe Hill mine and project, referred to as K.Hill, the Otse manganese prospect and the Lobatse manganese prospect, both of which have seen historical mining activities.

About SRK

SRK is an independent global mining consulting firm that is owned by its worldwide employees and specialises in technical studies that deliver added value and reduced risk to all stakeholders. Website: https://www.srk.co.uk/en

About Tetra Tech

Tetra Tech is a leading provider of high-end consulting and engineering services for projects globally. With 21,000 associates and 450 offices worldwide, Tetra Tech provides clear solutions to complex problems in water, environment, infrastructure, resource management, energy, and international development. For more information about Tetra Tech, please visit www.tetratech.com

On behalf of the Board of Directors of Giyani Metals Corp.

Jonathan Henry, Executive Chair

Contact:

Jonathan Henry

Executive Chair

+44 7798 801 783

George Donne

VP Business Development

+44 7866 591 897

Neither the TSX Venture Exchange (the "TSXV") nor its Regulation Services Provider (as that term is defined in the policies of the TSXV) accepts responsibility for the adequacy or accuracy of this news release.

The securities described herein have not been registered under the United States Securities Act of 1933, as amended (the "U.S. Securities Act"), or any state securities laws, and accordingly, may not be offered or sold to, or for the account or benefit of, persons in the United States or "U.S. persons," as such term is defined in Regulation S promulgated under the U.S. Securities Act ("U.S. Persons"), except in compliance with the registration requirements of the U.S. Securities Act and applicable state securities requirements or pursuant to exemptions therefrom. This press release does not constitute an offer to sell or a solicitation of an offer to buy any of the Company's securities to, or for the account of benefit of, persons in the United States or U.S. Persons.

Forward Looking Information

This press release contains "forward-looking information" within the meaning of applicable Canadian securities legislation. All statements in this news release, other than statements of historical fact, that address events or developments that Giyani expects to occur, are "forward-looking statements". Forward-looking statements are statements that are not historical facts and are generally, but not always, identified by the words "expects", "does not expect", "plans", "anticipates", "does not anticipate", "believes", "intends", "estimates", "projects", "potential", "scheduled", "forecast", "budget" and similar expressions, or that events or conditions "will", "would", "may", "could", "should" or "might" occur. Specific forward-looking statements and forward-looking information herein includes completion of receipt of TSXV approval for the private placement and completion of the private placement.

All such forward-looking statements are based on the opinions and estimates of the relevant management as of the date such statements are made and are subject to certain assumptions, important risk factors and uncertainties, many of which are beyond Giyani's ability to control or predict. Forward-looking statements are necessarily based on estimates and assumptions that are inherently subject to known and unknown risks, uncertainties and other factors that may cause actual results, level of activity, performance or achievements to be materially different from those expressed or implied by such forward-looking statements. In the case of Giyani, these facts include their anticipated operations in future periods, planned exploration and development of its properties, and plans related to its business and other matters that may occur in the future. This information relates to analyses and other information that is based on expectations of future performance and planned work programs.

Forward-looking information is subject to a variety of known and unknown risks, uncertainties and other factors which could cause actual events or results to differ from those expressed or implied by the forward-looking information, including, without limitation: inherent exploration hazards and risks; risks related to exploration and development of natural resource properties; uncertainty in Giyani's ability to obtain funding; commodity price fluctuations; recent market events and conditions; risks related to the uncertainty of mineral resource calculations and the inclusion of inferred mineral resources in economic estimation; risks in how the world-wide economic and social impact of COVID-19 is managed; risks related to governmental regulations; risks related to obtaining necessary licences and permits; risks related to their business being subject to environmental laws and regulations; risks related to their mineral properties being subject to prior unregistered agreements, transfers, or claims and other defects in title; risks relating to competition from larger companies with greater financial and technical resources; risks relating to the inability to meet financial obligations under agreements to which they are a party; ability to recruit and retain qualified personnel; and risks related to their directors and officers becoming associated with other natural resource companies which may give rise to conflicts of interests. This list is not exhaustive of the factors that may affect Giyani's forward-looking information. Should one or more of these risks and uncertainties materialize, or should underlying assumptions prove incorrect, actual results may vary materially from those described in the forward-looking information or statements.

Giyani's forward-looking information is based on the reasonable beliefs, expectations and opinions of their respective management on the date the statements are made, and Giyani does not assume any obligation to update forward looking information if circumstances or management's beliefs, expectations or opinions change, except as required by law. For the reasons set forth above, investors should not place undue reliance on forward-looking information. For a complete discussion with respect to Giyani and risks associated with forward-looking information and forward-looking statements, please refer to Giyani's Annual Information Form, all of which are filed on SEDAR at www.sedar.com.

¹ Based on a US$:C$ exchange rate of 1.35

² Source: Freightos Limited