Yahoo Finance

Yahoo Finance Foot Locker (FL) Stock Up 8.7% on Q3 Earnings and Sales Beat

Foot Locker, Inc. FL posted better-than-expected results for third-quarter fiscal 2022, wherein the top and the bottom line surpassed the Zacks Consensus Estimate. FL delivered the 10th straight earnings beat in the reported quarter.

Driven by strong third-quarter results, robust demand and a healthy inventory, management raised the outlook for fiscal 2022. For the holiday season, management remains encouraged by the business momentum. Management expects a robust launch lineup, comprising the key releases of Jordan Retros, follow-up launches of Melo Ball 2, new Crocs collabs among others. Foot Locker’s FLX membership program and omnichannel capabilities appear encouraging.

Shares of this athletic footwear and apparel retailer rallied 8.7% during the trading session on Nov 18. Over the past three months, the stock has increased 14.5% compared with the industry’s 2.5% decline.

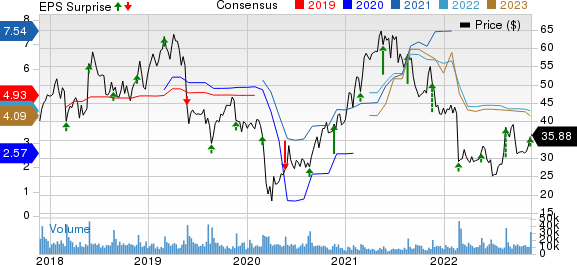

Q3 Metrics

The athletic shoes and apparel retailer posted adjusted earnings of $1.27 per share, which surpassed the Zacks Consensus Estimate of 44 cents. The bottom line decreased from $1.74 per share recorded in the prior-year fiscal quarter.

Foot Locker, Inc. Price, Consensus and EPS Surprise

Foot Locker, Inc. price-consensus-eps-surprise-chart | Foot Locker, Inc. Quote

Total sales of $2,173 million dipped 0.7% from the prior fiscal year’s level but came above the consensus estimate of $2,112 million. Excluding the foreign-currency fluctuation impacts, total sales grew 3.3%.

Comparable-store sales (comps) inched up 0.8% in the fiscal third quarter, backed by strong demand, brand-diversification efforts and better access to high-quality inventory. The non-Nike sales across the company’s core banners grew mid-single digits. By category, footwear comped up in the low-single digits, while apparel and accessories declined mid-single digits.

Comps in the company’s stores rose 4.7%. FL’s digital channel comped down 14.5% with the overall penetration at 16.3%, lower than the 19.8% witnessed last year, but above the 15.3% seen in 2019.

Foot Locker experienced sturdy demand signals within the basketball sneaker culture and kids. This trend is likely to continue into the fourth quarter. It saw outsized gains in brands like New Balance which was up about 70% in the reported quarter, Crocs and Converse, both were up over 25%, and UGG rose nearly 50%.

The company’s controlled brands performed impressively, increasing above 50% on strong fleece and outerwear performance by CSG and Locker brands. However, apparel remained soft in the quarter.

In North America, the overall comps decreased modestly 1.1%, with Foot Locker up high single digits on solid basketball trends and gains in the key back-to-school markets. Kids Foot Locker rose mid-single digits on broad-based strength across brands and solid marketing campaigns around the back-to-school season.

Champs Sports dropped in low-double digits, but is up versus 2019. WSS contributed nearly $162 million in sales with comps up in the low single digits in the reported quarter.

Further, comps in Europe grew 0.8%, backed by the strength in key markets, led by France, Italy and Spain. In Asia Pacific, comps surged 36.5%, driven by the easing of travel restrictions in certain Asian markets. Also, atmos witnessed strong trends with respect to the sneaker culture, contributing $40 million to sales and up double digits year over year on strong performance in Japan.

In addition, this Zacks Rank #3 (Hold) company’s community and Power Stores delivered healthy sales.

An Insight Into Margins

Foot Locker's gross-margin rate in the reported quarter dropped 270 basis points (bps) from the prior-year quarter’s tally. Increased markdowns on higher promotional activity across the industry, and modest supply-chain cost pressures hurt the metric.

The SG&A rate deleveraged nearly 60 bps due to increased labor, partly offset by early savings from its cost-optimization program.

Store Update

During the fiscal third quarter, Foot Locker opened 24 stores, and remodeled or relocated 23 outlets. FL closed 29 stores during the aforementioned period.

As of Oct 29, 2022, Foot Locker operated 2,794 stores across 28 countries in North America, Europe, Asia, Australia and New Zealand. Also, FL had 155 franchised stores operating in the Middle East and Asia.

For the fourth quarter of fiscal 2022, management expects to open roughly 20 stores. It has plans to shut down nearly 85 stores in the aforementioned period.

Other Financial Details

Foot Locker ended the fiscal third quarter with cash and cash equivalents of $351 million. Long-term debt and obligations under finance leases amounted to $448 million, while shareholders’ equity summed at $3,259 million. As of Oct 29, 2022, merchandise inventories were $1,685 million, up 29.5% from the year-earlier quarter’s end level.

During the reported quarter, Foot Locker paid out quarterly dividends of $37 million.

Outlook

For the fourth quarter of fiscal 2022, total sales are likely to drop 8-10%, with comps falling 6-8%. Gross margin is likely to be 29-29.3%, while SG&A rate is anticipated to deleverage 90-100 basis points to 23.3-23.4%. SG&A deleverage will be caused by the ongoing wage inflation and comps decline, partly offset by an expected savings of nearly $9 million from the cost-optimization program. Adjusted earnings are envisioned to be 45-53 cents a share for the fiscal fourth quarter.

Management expects sales to decline 4-5% in fiscal 2022 compared with the earlier view of falling 6-7%. Currency is likely to act as a deterrent. Comps are likely to drop 4-5% compared with the prior guidance of 8-9% on the back of solid demand, execution and access to inventory.

Gross margin is anticipated in the range of 31.7-31.8% compared with the prior view of 31.1-31.2%. The SG&A rate is forecast to be 22% compared with the 21.3-21.4% rate guided earlier due to labor inflation, partly offset by cost optimization.

FL now envisions adjusted earnings per share of $4.42-$4.50 for the full fiscal compared with $4.25-$4.45 projected earlier. Management predicts capEx at $275 million for fiscal 2022.

At the end of the fiscal year, Foot Locker expects the inventories to remain up year over year, positioning the company strong to start in 2023. Management expects to conclude the year with a greater mix of Nike sales than earlier anticipated in addition to the robust demand across its portfolio.

3 Top Retail Stocks

We highlighted three better-ranked stocks in the Retail - Wholesale sector, namely Tecnoglass TGLS, Ulta Beauty ULTA and CVS Health CVS.

Tecnoglass manufactures and sells architectural glass and aluminum products for the residential and commercial construction industries. TGLS currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Tecnoglass’ current financial-year sales and earnings per share suggests growth of 28.2% and 47.7%, respectively, from the corresponding year-ago reported figures. TGLS has a trailing four-quarter earnings surprise of 24.4%, on average.

Ulta Beauty, a leading beauty retailer in the United States, currently has a Zacks Rank #2 (Buy). ULTA has a trailing four-quarter earnings surprise of 49.8%, on average.

The Zacks Consensus Estimate for Ulta Beauty’s current financial-year sales suggests growth of 10.4% from the corresponding year-ago reported figure. ULTA has an expected EPS growth rate of 10.7% for three-five years.

CVS Health, a pharmacy innovation company with integrated offerings across the entire spectrum of pharmacy care, currently has a Zacks Rank of 2. CVS has a trailing four-quarter earnings surprise of 6.7%, on average. The stock has risen 7% in the past three months.

The Zacks Consensus Estimate for CVS Health’s current financial-year sales and earnings per share suggests growth of 6.6% and 1.1%, respectively, from the corresponding year-ago reported numbers. CVS has an expected EPS growth rate of 7.7% for three-five years.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

CVS Health Corporation (CVS) : Free Stock Analysis Report

Foot Locker, Inc. (FL) : Free Stock Analysis Report

Ulta Beauty Inc. (ULTA) : Free Stock Analysis Report

Tecnoglass Inc. (TGLS) : Free Stock Analysis Report