Yahoo Finance

Yahoo Finance Exploring Undervalued Small Caps With Insider Action In June 2024 in Hong Kong

As global markets navigate through a period of fluctuating inflation rates and interest rate expectations, the Hong Kong small-cap sector presents a unique landscape for investors seeking value. Amidst broader market dynamics, understanding the intrinsic qualities that define promising small-cap stocks—such as robust insider buying—can offer insightful perspectives in June 2024.

Top 10 Undervalued Small Caps With Insider Buying In Hong Kong

Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

Xtep International Holdings | 11.2x | 0.8x | 40.40% | ★★★★★☆ |

Tian Lun Gas Holdings | 7.2x | 0.4x | 22.22% | ★★★★★☆ |

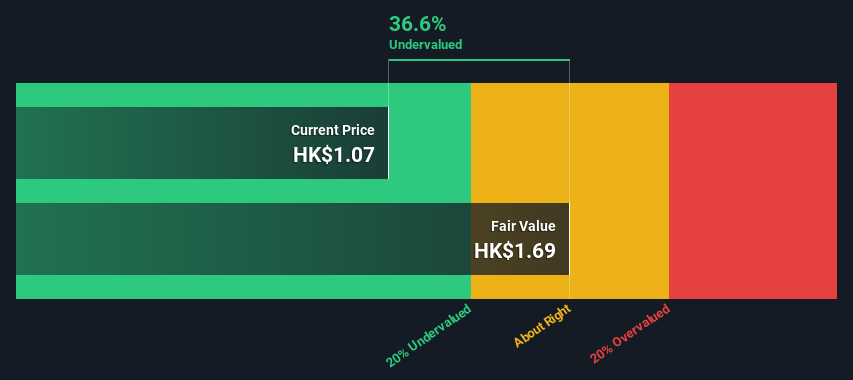

Far East Consortium International | NA | 0.3x | 36.63% | ★★★★★☆ |

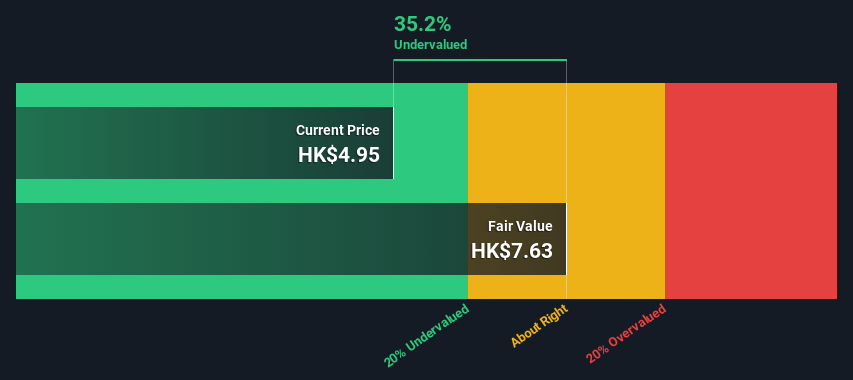

Nissin Foods | 15.3x | 1.4x | 35.02% | ★★★★☆☆ |

China Leon Inspection Holding | 9.7x | 0.7x | 28.65% | ★★★★☆☆ |

China Lesso Group Holdings | 4.2x | 0.3x | 5.22% | ★★★★☆☆ |

Transport International Holdings | 11.0x | 0.6x | 45.53% | ★★★★☆☆ |

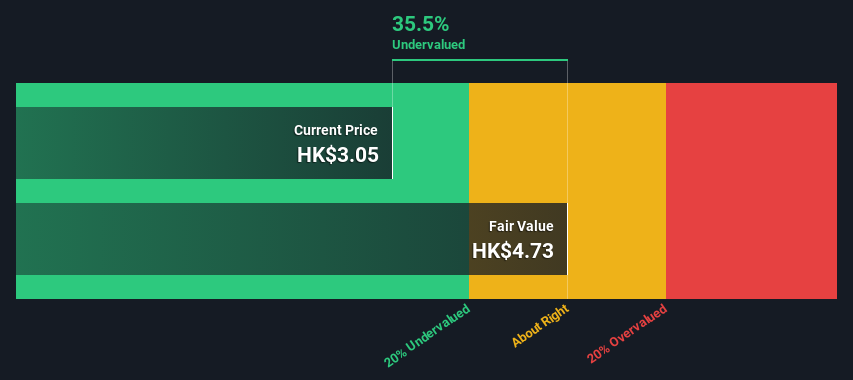

Abbisko Cayman | NA | 96.3x | 35.86% | ★★★★☆☆ |

Giordano International | 8.8x | 0.8x | 35.02% | ★★★☆☆☆ |

China Overseas Grand Oceans Group | 3.1x | 0.1x | -11.41% | ★★★☆☆☆ |

Underneath we present a selection of stocks filtered out by our screen.

Nissin Foods

Simply Wall St Value Rating: ★★★★☆☆

Overview: Nissin Foods is a company primarily engaged in the production and sale of instant noodles, with operations focused in Mainland China, Hong Kong, and other parts of Asia.

Operations: Mainland China and Hong Kong, along with other Asian regions, are significant contributors to the company's revenue, generating HK$2.47 billion and HK$1.68 billion respectively. The firm has observed a gross profit margin trend fluctuating between 30% to approximately 34% over recent periods.

PE: 15.3x

Nissin Foods, a lesser-known entity in Hong Kong's market, recently saw insider confidence bolstered as Kiyotaka Ando acquired 155,430 shares, signaling strong belief in the company’s prospects. This move aligns with a robust financial trajectory indicated by a 7.34% forecasted annual earnings growth. Additionally, the appointment of experienced executives like Mr. Kiyoshi Matsuura underscores strategic leadership enhancements ahead of future challenges and opportunities. With recent dividends increased to 15.82 HK cents per share reflecting solid financial health and shareholder commitment, Nissin positions itself as an intriguing consideration amidst undervalued entities in Hong Kong’s vibrant market landscape.

Take a closer look at Nissin Foods' potential here in our valuation report.

Assess Nissin Foods' past performance with our detailed historical performance reports.

Abbisko Cayman

Simply Wall St Value Rating: ★★★★☆☆

Overview: Abbisko Cayman is a company focused on the development of innovative medicines, with a market capitalization of approximately CN¥19.06 million.

Operations: The entity consistently records a gross profit margin of 100%, indicating that it generates CN¥19.06 million from its core operations without the cost of goods sold. However, it faces substantial operating expenses and R&D costs, which have led to persistent net losses, with the latest being CN¥431.58 million as of mid-2024.

PE: -4.3x

Abbisko Cayman, despite its limited revenue of CN¥19M and non-profitable outlook, recently showcased its potential through insider confidence; executives bought shares in April 2024, signaling belief in their strategic direction. This gesture coincides with the U.S. FDA's Orphan Drug Designation for their FGFR4 inhibitor, irpagratinib, aimed at treating rare liver cancer—highlighting both the company’s innovative edge and niche market focus. While facing declining earnings forecasts, these developments could suggest a turnaround trajectory as they continue to push boundaries in biopharmaceuticals.

Unlock comprehensive insights into our analysis of Abbisko Cayman stock in this valuation report.

Review our historical performance report to gain insights into Abbisko Cayman's's past performance.

Far East Consortium International

Simply Wall St Value Rating: ★★★★★☆

Overview: Far East Consortium International is a diversified company engaged in property development and investment, hotel operations, and gaming across multiple regions including Hong Kong, Australia, the UK, and Southeast Asia.

Operations: Analyzing the financial trends from 2013 to 2024, the company experienced fluctuations in gross profit margin, ranging from 33.21% in June 2013 to a peak of approximately 54.81% by September 2017, before stabilizing around the mid-30% range towards the latest data point. Notably, revenue also saw significant growth during this period, increasing from HK$4.18 billion in June 2013 to HK$9.61 billion by September 2024.

PE: -18.1x

Recently, Far East Consortium International has demonstrated insider confidence, with Chairman & CEO Tat Cheong Chiu acquiring 5.89 million shares for US$7.03 million, signaling strong belief in the company's prospects. This move is particularly noteworthy given that financial assessments reveal some concerns; earnings barely cover interest payments and past shareholder dilution. However, the company's funding strategy avoids customer deposits, relying solely on external borrowing—considered higher risk but possibly reflective of an assertive growth strategy. This blend of insider optimism and complex financial structure suggests a nuanced opportunity within Hong Kong’s lesser-known equities.

Turning Ideas Into Actions

Dive into all 16 of the Undervalued Small Caps With Insider Buying we have identified here.

Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Seeking Other Investments?

Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include SEHK:1475 SEHK:2256 and SEHK:35.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com