Yahoo Finance

Yahoo Finance Exelixis (EXEL) Q2 Earnings & Sales Beat, Cabometyx Shines

Exelixis, Inc. EXEL delivered better-than-expected results for second-quarter 2019, wherein both earnings and revenues beat estimates on strong performance by Cabometyx.

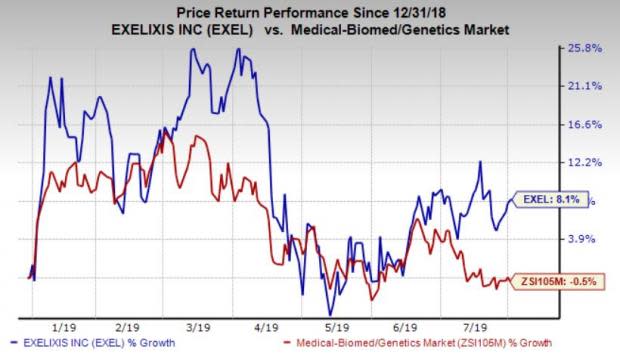

The company’s shares have gained 8.1% in the year so far against the industry’s decline of 0.5%.

Exelixis reported earnings of 25 cents, easily beating the Zacks Consensus Estimate of 23 cents. However, the bottom line declined from 28 cents in the year-ago quarter.

Net revenues came in at $240.3 million, up from $186.1 million in the year-ago quarter. The top line also surpassed the Zacks Consensus Estimate of $228.97 million.

Quarter in Detail

Net product revenues came in at $193.7 million, up 32.8% from the year-ago quarter, driven by continued growth of Cabometyx in the United States for the treatment of advanced renal cell carcinoma (RCC).

In April 2016, the FDA approved a tablet formulation of cabozantinib (distinct from the capsule form), under the brand name Cabometyx, for the treatment of advanced RCC in patients, who have received prior anti-angiogenic therapy. The company also expanded the drug’s label for the treatment of previously-untreated advanced RCC in December 2017. Cabometyx received another FDA approval for the treatment of patients with hepatocellular carcinoma (HCC) in January 2019. The launch of the drug for this indication in the United States also boosted sales.

Cabometyx generated $189 million of net product revenues. Patient demand grew 26% year over year and 9% sequentially, driven by both RCC and HCC. Prescriber base grew by 45%.

Cometriq (cabozantinib capsules), for the treatment of medullary thyroid cancer, generated $4.7 million in net product revenues.

Total collaboration revenues were $46.6 million, up from $40.3 million in the year-ago quarter, primarily owing to the recognition of a $20.0-million milestone from Daiichi Sankyo Company, Limited (Daiichi Sankyo) for the launch of Minnebro (esaxerenone) tablets as a treatment for patients with hypertension in Japan.

In the reported quarter, research and development expenses increased 92.7% to $81.9 million owing to high clinical trial costs, license and other collaboration costs, personnel expenses and stock-based compensation. Selling, general and administrative (SG&A) expenses were $58.8 million, up 13.3% year over year, driven by increase in personnel expenses and stock-based compensation.

Pipeline Update

The pipeline progress in the year so far has been encouraging.

In April, CheckMate 9ER, the phase III trial evaluating the combination of cabozantinib and Opdivo versus Pfizer’s PFE Sutent in patients with previously-untreated advanced or metastatic RCC, completed enrollment. The study was sponsored by Bristol-Myers Squibb Company BMY and co-funded by Exelixis, and partners Ipsen and Takeda. Results are expected by early 2020.

Exelixis initiated a multi-center, randomized, double-blinded, controlled phase III study, COSMIC-313. The study is evaluating Cabometyx in combination with Opdivo and Yervoy versus Opdivo and Yervoy in patients with previously untreated advanced RCC. The primary endpoint of the trial is progression-free survival, and the secondary endpoints are overall survival and objective response rate.

Exelixis announced that amendments have been made to its multi-center, open-label, phase Ib study, COSMIC-021, evaluating Cabometyx in combination with Roche’s RHHBY Tecentriq in patients with locally advanced or metastatic solid tumors. Two original cohorts are being expanded and four cohorts being included in the COSMIC-021 study. The original immunotherapy-refractory non-small cell lung cancer (NSCLC) and metastatic castration-resistant prostate cancer (CRPC) cohorts are being expanded to 80 patients each, based on encouraging early efficacy and safety data. Also, four cohorts, consisting of two expansion and two exploratory cohorts, are being added to the study. The two new expansion cohorts will evaluate the above-mentioned combination in patients with metastatic CRPC, who have received prior enzalutamide or abiraterone therapy, with or without prior docetaxel therapy.

Last month, Exelixis inked an exclusive option and license agreement with Aurigene, a biotechnology company from India focusing on oncology and inflammatory disorders, to in-license up to six oncology programs from the latter. Per the terms, Exelixis will make an upfront payment of $10.0 million for exclusive options to license three pre-existing programs.

2019 Guidance

R&D expenses are expected between $330 million and $350 million and SG&A expenses between $220 million and $240 million.

Our Take

Exelixis’ second-quarter results were impressive despite increasing competition from Pfizer’s Inlyta. The drug gained market share throughout the second quarter for the RCC indication. The initial traction for the HCC indication in the second and third-line setting was encouraging as well.

The company ended the quarter with 34% market share, backed by its broad label for advanced RCC. We expect a strong performance in the second half of 2019 as well.

Zacks Rank

Exelixis currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Looking for Stocks with Skyrocketing Upside?

Zacks has just released a Special Report on the booming investment opportunities of legal marijuana.

Ignited by new referendums and legislation, this industry is expected to blast from an already robust $6.7 billion to $20.2 billion in 2021. Early investors stand to make a killing, but you have to be ready to act and know just where to look.

See the pot trades we're targeting>>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Pfizer Inc. (PFE) : Free Stock Analysis Report

Roche Holding AG (RHHBY) : Free Stock Analysis Report

Bristol-Myers Squibb Company (BMY) : Free Stock Analysis Report

Exelixis, Inc. (EXEL) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research