Yahoo Finance

Yahoo Finance Energy Stock Earnings Lineup for Nov 5: FANG, DVN & More

The Oil/Energy sector is more than halfway through the Q3 earnings season, with 55.2% S&P 500 members having reported results as of Thursday, Oct 31. Another handful of companies from the space is likely to come up with quarterly numbers by the end of this week. Before going into the details of the upcoming releases, let’s take a look at the factors affecting quarterly results and the report card so far.

A Combination of Lower Oil & Gas Prices

So, how does the price of oil and gas compare with the year-ago period?

According to the U.S. Energy Information Administration, WTI prices started the third quarter of 2018 at around $74 per barrel and exited the period at $73 per barrel. This year, prices were $59 a barrel at the start of the third quarter and fell to $55 at the end of September.

The news is not rosy on the natural gas front either.

In Q3 of last year, natural gas prices were around $2.85 per MMBtu in the beginning and rose steadily to end September at more than $3 per MMBtu. Coming to 2019, the fuel was trading at $2.25 per MMBtu in the beginning of July and struggled throughout the quarter to end at $2.33 per MMBtu.

Companies Across the Board to Have Suffered

Taking into account the commodity price drop, the picture looks rather downbeat for the Q3 earnings season and is validated by the sector’s dismal earnings picture so far. Even biggies like ExxonMobil XOM, Chevron CVX and Royal Dutch Shell RDS.A bore the brunt of weaker oil and gas prices as they fell short of year-ago earnings despite beating profit expectations.

Per the latest Earnings Trends, Energy is one of the three sectors likely to have experienced double-digit earnings decline in the third quarter. Per our expectations, the sector’s earnings are likely to fall 34.8% from third-quarter 2018 on 3.3% lower revenues.

For the companies that have already reported, total earnings are down 23.8% from the same period last year on 0.4% lower revenues, with 50% positive earnings surprises and 37.5% beating revenue estimates.

Key Releases

Given the bleak year-over-year backdrop, let’s take a glance at how four energy players are placed ahead of their third-quarter results slated for release on Nov 5.

Our proprietary model clearly indicates that a company needs to have the right combination of two key ingredients — a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) — to increase the odds of an earnings beat.

You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

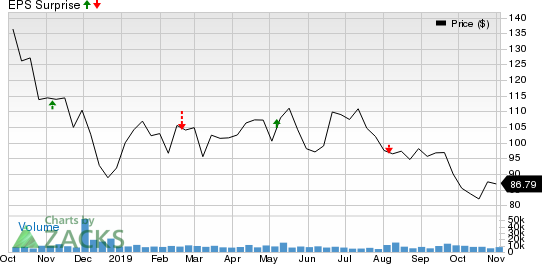

Diamondback Energy, Inc. FANG: Diamondback, a leading Permian Basin oil producer, is slated to report quarterly results after the closing bell. The company came up with weaker-than-expected earnings in the last reported quarter, hurt by low natural gas price realizations. As far as earnings surprises are concerned, the firm displays a mixed record. It surpassed the Zacks Consensus Estimate in two of the last four quarters. This is depicted in the graph below:

The current Zacks Consensus Estimate for the to-be-reported quarter is a profit of $1.73 per share on revenues of $1.1 billion. This indicates year-over-year earnings and revenue growth of 3.6% and 95.3%, respectively.

Our proven model does not conclusively predict an earnings beat for Diamondback this time around, as it has an Earnings ESP of -0.63% and a Zacks Rank #3. (Read More: Diamondback to Report Q3 Earnings: What's in Store?)

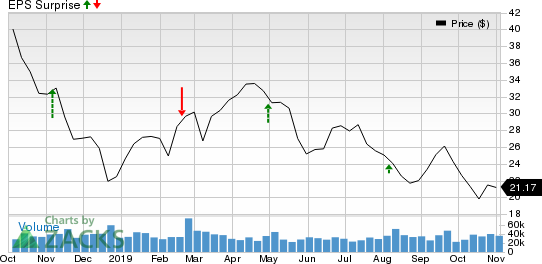

Devon Energy Corp. DVN: Devon Energy, with oil and gas operations mainly concentrated on the onshore areas of North America, is also set to report quarterly results after the closing bell. In the last reported quarter, the Oklahoma City, OK-based company beat the consensus mark on higher oil production and lower expenses. Regarding earnings surprises, the North American upstream operator is on a solid footing, having gone past the Zacks Consensus Estimate in three of the last four reports. This is depicted in the graph below:

The current Zacks Consensus Estimate for the to-be-reported quarter is a profit of 19 cents per share on revenues of $1.6 billion. This indicates a year-over-year earnings and revenue decline of 69.8% and 39.2%, respectively.

Our proven model does not conclusively predict an earnings beat for Devon Energy this time around, as it has an Earnings ESP of -3.48% and a Zacks Rank #3. (Read More: What's in the Offing for Devon Energy's Q3 Earnings?)

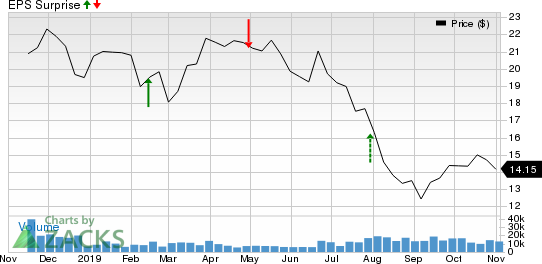

Parsley Energy, Inc. PE: Parsley Energy, whose core operations are focused on the prolific Permian Basin, is slated to report quarterly results after the closing bell. The company came up with better-than-expected earnings in the last reported quarter on strong production. As far as earnings surprises are concerned, the firm displays a mixed record. It surpassed the Zacks Consensus Estimate in two of the last four quarters. This is depicted in the graph below:

The current Zacks Consensus Estimate for the to-be-reported quarter is a profit of 34 cents per share on revenues of $500.4 million. This indicates a year-over-year earnings and revenue decline of 24.4% and 2.1%, respectively.

Our proven model predicts an earnings beat for Parsley Energy this time around, as it has an Earnings ESP of +1.06% and a Zacks Rank #3.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Equitrans Midstream Corporation ETRN: Equitrans Midstream, which spun off from EQT Corporation in late 2018, is set to unveil quarterly results before the opening bell. In the last reported quarter, the energy infrastructure provider with a premier asset footprint in the Appalachian Basin beat the consensus mark on strong natural gas gathering volumes. Regarding earnings surprises, the Canonsburg, PA-based company has a mixed record, having gone past the Zacks Consensus Estimate in two of the last four reports. This is depicted in the graph below:

The current Zacks Consensus Estimate for the to-be-reported quarter is a profit of 42 cents per share on revenues of $409 million.

Our proven model does not conclusively predict an earnings beat for Equitrans Midstream this time around, as it has an Earnings ESP of 0.00% and a Zacks Rank #3.

Biggest Tech Breakthrough in a Generation

Be among the early investors in the new type of device that experts say could impact society as much as the discovery of electricity. Current technology will soon be outdated and replaced by these new devices. In the process, it’s expected to create 22 million jobs and generate $12.3 trillion in activity.

A select few stocks could skyrocket the most as rollout accelerates for this new tech. Early investors could see gains similar to buying Microsoft in the 1990s. Zacks’ just-released special report reveals 8 stocks to watch. The report is only available for a limited time.

See 8 breakthrough stocks now>>

Click to get this free report Chevron Corporation (CVX) : Free Stock Analysis Report Exxon Mobil Corporation (XOM) : Free Stock Analysis Report Royal Dutch Shell PLC (RDS.A) : Free Stock Analysis Report Devon Energy Corporation (DVN) : Free Stock Analysis Report Diamondback Energy, Inc. (FANG) : Free Stock Analysis Report Parsley Energy, Inc. (PE) : Free Stock Analysis Report Equitrans Midstream Corporation (ETRN) : Free Stock Analysis Report To read this article on Zacks.com click here. Zacks Investment Research