Yahoo Finance

Yahoo Finance eCargo Holdings (ASX:ECG) Is Carrying A Fair Bit Of Debt

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies eCargo Holdings Limited (ASX:ECG) makes use of debt. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

See our latest analysis for eCargo Holdings

What Is eCargo Holdings's Debt?

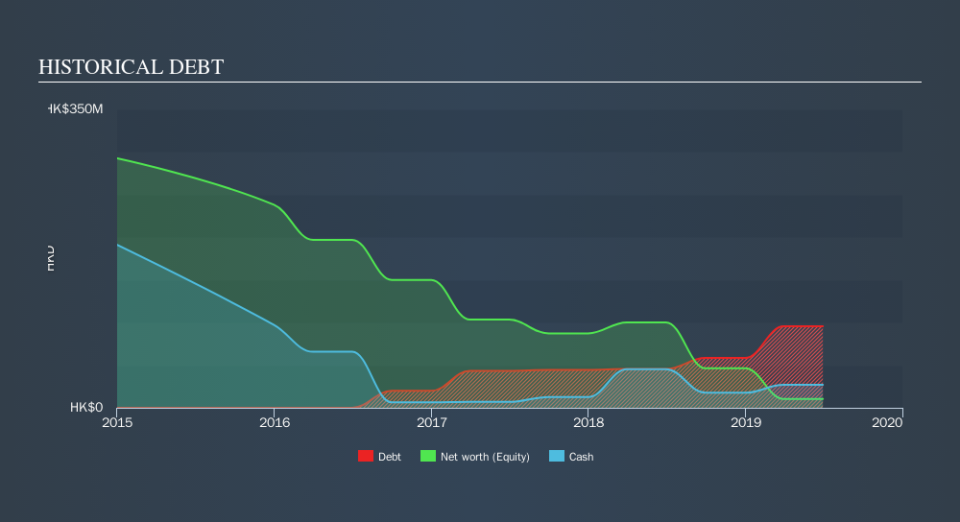

As you can see below, at the end of June 2019, eCargo Holdings had HK$95.7m of debt, up from HK$45.5m a year ago. Click the image for more detail. However, it also had HK$27.0m in cash, and so its net debt is HK$68.7m.

How Healthy Is eCargo Holdings's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that eCargo Holdings had liabilities of HK$61.1m due within 12 months and liabilities of HK$121.8m due beyond that. Offsetting this, it had HK$27.0m in cash and HK$32.3m in receivables that were due within 12 months. So its liabilities total HK$123.5m more than the combination of its cash and short-term receivables.

This deficit is considerable relative to its market capitalization of HK$151.8m, so it does suggest shareholders should keep an eye on eCargo Holdings's use of debt. This suggests shareholders would heavily diluted if the company needed to shore up its balance sheet in a hurry. When analysing debt levels, the balance sheet is the obvious place to start. But it is eCargo Holdings's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Over 12 months, eCargo Holdings saw its revenue drop to HK$139m, which is a fall of 9.8%. That's not what we would hope to see.

Caveat Emptor

Over the last twelve months eCargo Holdings produced an earnings before interest and tax (EBIT) loss. Indeed, it lost a very considerable HK$25m at the EBIT level. When we look at that and recall the liabilities on its balance sheet, relative to cash, it seems unwise to us for the company to have any debt. So we think its balance sheet is a little strained, though not beyond repair. We would feel better if it turned its trailing twelve month loss of-HK$85.0m into a profit. So to be blunt we do think it is risky. When we look at a riskier company, we like to check how their profits (or losses) are trending over time. Today, we're providing readers this interactive graph showing how eCargo Holdings's profit, revenue, and operating cashflow have changed over the last few years.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.