Yahoo Finance

Yahoo Finance Is easyJet (LON:EZJ) A Risky Investment?

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about. It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, easyJet plc (LON:EZJ) does carry debt. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

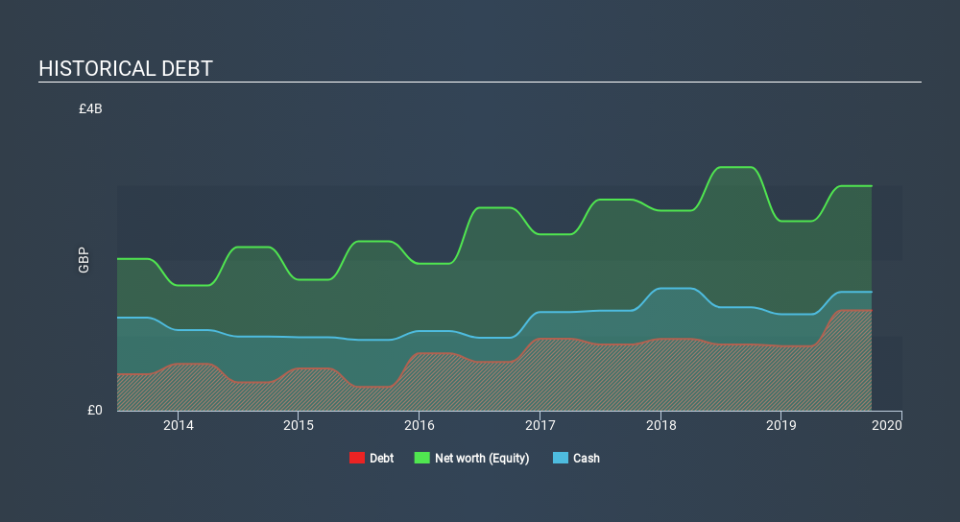

See our latest analysis for easyJet

What Is easyJet's Debt?

As you can see below, at the end of September 2019, easyJet had UK£1.33b of debt, up from UK£879.0m a year ago. Click the image for more detail. But it also has UK£1.58b in cash to offset that, meaning it has UK£245.0m net cash.

How Strong Is easyJet's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that easyJet had liabilities of UK£2.67b due within 12 months and liabilities of UK£2.51b due beyond that. Offsetting this, it had UK£1.58b in cash and UK£149.0m in receivables that were due within 12 months. So its liabilities total UK£3.45b more than the combination of its cash and short-term receivables.

When you consider that this deficiency exceeds the company's UK£2.54b market capitalization, you might well be inclined to review the balance sheet intently. In the scenario where the company had to clean up its balance sheet quickly, it seems likely shareholders would suffer extensive dilution. easyJet boasts net cash, so it's fair to say it does not have a heavy debt load, even if it does have very significant liabilities, in total.

The modesty of its debt load may become crucial for easyJet if management cannot prevent a repeat of the 21% cut to EBIT over the last year. Falling earnings (if the trend continues) could eventually make even modest debt quite risky. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if easyJet can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. While easyJet has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Looking at the most recent three years, easyJet recorded free cash flow of 25% of its EBIT, which is weaker than we'd expect. That weak cash conversion makes it more difficult to handle indebtedness.

Summing up

While easyJet does have more liabilities than liquid assets, it also has net cash of UK£245.0m. Despite the cash, we do find easyJet's EBIT growth rate concerning, so we're not particularly comfortable with the stock. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. For example, we've discovered 3 warning signs for easyJet that you should be aware of before investing here.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.