Yahoo Finance

Yahoo Finance How Does Treasury Wine Estates's (ASX:TWE) P/E Compare To Its Industry, After The Share Price Drop?

Unfortunately for some shareholders, the Treasury Wine Estates (ASX:TWE) share price has dived 34% in the last thirty days. Even longer term holders have taken a real hit with the stock declining 23% in the last year.

Assuming nothing else has changed, a lower share price makes a stock more attractive to potential buyers. In the long term, share prices tend to follow earnings per share, but in the short term prices bounce around in response to short term factors (which are not always obvious). The implication here is that long term investors have an opportunity when expectations of a company are too low. Perhaps the simplest way to get a read on investors' expectations of a business is to look at its Price to Earnings Ratio (PE Ratio). Investors have optimistic expectations of companies with higher P/E ratios, compared to companies with lower P/E ratios.

View our latest analysis for Treasury Wine Estates

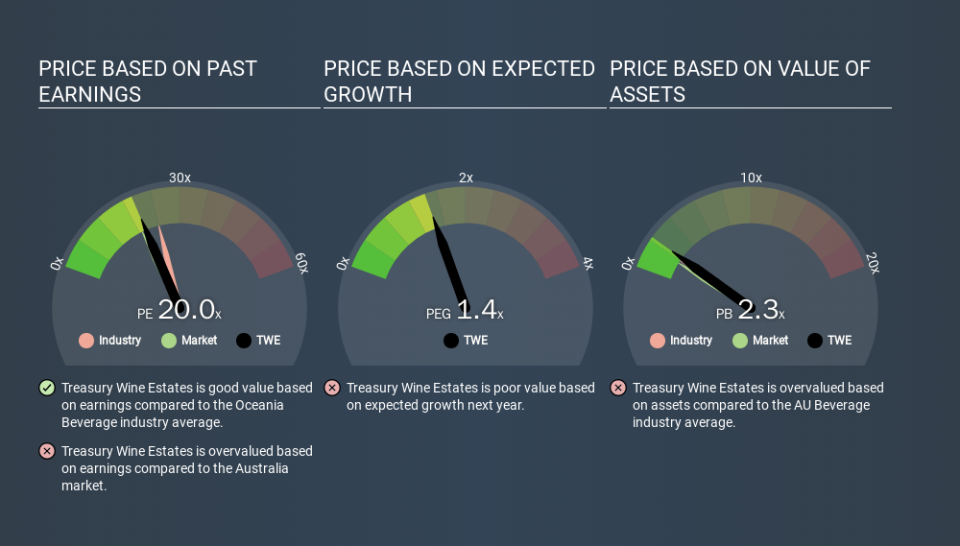

How Does Treasury Wine Estates's P/E Ratio Compare To Its Peers?

Treasury Wine Estates's P/E of 20.03 indicates relatively low sentiment towards the stock. The image below shows that Treasury Wine Estates has a lower P/E than the average (23.9) P/E for companies in the beverage industry.

This suggests that market participants think Treasury Wine Estates will underperform other companies in its industry. Many investors like to buy stocks when the market is pessimistic about their prospects. You should delve deeper. I like to check if company insiders have been buying or selling.

How Growth Rates Impact P/E Ratios

Earnings growth rates have a big influence on P/E ratios. When earnings grow, the 'E' increases, over time. And in that case, the P/E ratio itself will drop rather quickly. So while a stock may look expensive based on past earnings, it could be cheap based on future earnings.

Treasury Wine Estates's earnings per share grew by -8.0% in the last twelve months. And it has improved its earnings per share by 19% per year over the last three years.

Don't Forget: The P/E Does Not Account For Debt or Bank Deposits

One drawback of using a P/E ratio is that it considers market capitalization, but not the balance sheet. That means it doesn't take debt or cash into account. In theory, a company can lower its future P/E ratio by using cash or debt to invest in growth.

Such spending might be good or bad, overall, but the key point here is that you need to look at debt to understand the P/E ratio in context.

Treasury Wine Estates's Balance Sheet

Treasury Wine Estates's net debt is 8.7% of its market cap. The market might award it a higher P/E ratio if it had net cash, but its unlikely this low level of net borrowing is having a big impact on the P/E multiple.

The Verdict On Treasury Wine Estates's P/E Ratio

Treasury Wine Estates trades on a P/E ratio of 20.0, which is fairly close to the AU market average of 18.9. When you consider the modest EPS growth last year (along with some debt), it seems the market thinks the growth is sustainable. What can be absolutely certain is that the market has become significantly less optimistic about Treasury Wine Estates over the last month, with the P/E ratio falling from 30.5 back then to 20.0 today. For those who prefer to invest with the flow of momentum, that might be a bad sign, but for a contrarian, it may signal opportunity.

Investors have an opportunity when market expectations about a stock are wrong. People often underestimate remarkable growth -- so investors can make money when fast growth is not fully appreciated. So this free visualization of the analyst consensus on future earnings could help you make the right decision about whether to buy, sell, or hold.

Of course you might be able to find a better stock than Treasury Wine Estates. So you may wish to see this free collection of other companies that have grown earnings strongly.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.