Yahoo Finance

Yahoo Finance Does Funko (NASDAQ:FNKO) Deserve A Spot On Your Watchlist?

Investors are often guided by the idea of discovering 'the next big thing', even if that means buying 'story stocks' without any revenue, let alone profit. Unfortunately, these high risk investments often have little probability of ever paying off, and many investors pay a price to learn their lesson. Loss-making companies are always racing against time to reach financial sustainability, so investors in these companies may be taking on more risk than they should.

If this kind of company isn't your style, you like companies that generate revenue, and even earn profits, then you may well be interested in Funko (NASDAQ:FNKO). Even if this company is fairly valued by the market, investors would agree that generating consistent profits will continue to provide Funko with the means to add long-term value to shareholders.

See our latest analysis for Funko

How Quickly Is Funko Increasing Earnings Per Share?

The market is a voting machine in the short term, but a weighing machine in the long term, so you'd expect share price to follow earnings per share (EPS) outcomes eventually. That means EPS growth is considered a real positive by most successful long-term investors. Funko's shareholders have have plenty to be happy about as their annual EPS growth for the last 3 years was 42%. That sort of growth rarely ever lasts long, but it is well worth paying attention to when it happens.

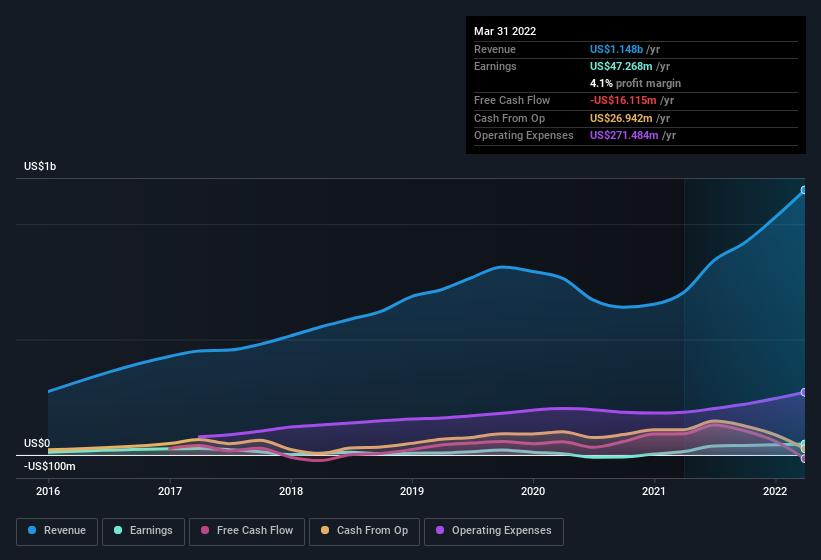

Careful consideration of revenue growth and earnings before interest and taxation (EBIT) margins can help inform a view on the sustainability of the recent profit growth. Funko shareholders can take confidence from the fact that EBIT margins are up from 6.1% to 8.6%, and revenue is growing. That's great to see, on both counts.

In the chart below, you can see how the company has grown earnings and revenue, over time. To see the actual numbers, click on the chart.

Fortunately, we've got access to analyst forecasts of Funko's future profits. You can do your own forecasts without looking, or you can take a peek at what the professionals are predicting.

Are Funko Insiders Aligned With All Shareholders?

It's said that there's no smoke without fire. For investors, insider buying is often the smoke that indicates which stocks could set the market alight. Because often, the purchase of stock is a sign that the buyer views it as undervalued. However, insiders are sometimes wrong, and we don't know the exact thinking behind their acquisitions.

We did see some selling in the last twelve months, but that's insignificant compared to the whopping US$1.7m that the Independent Chairman of the Board, Charles Denson spent acquiring shares. The average price paid was about US$17.22. It's not often you see purchases like this and so it should be on the radar of everyone who follows Funko.

It's commendable to see that insiders have been buying shares in Funko, but there is more evidence of shareholder friendly management. To be specific, the CEO is paid modestly when compared to company peers of the same size. Our analysis has discovered that the median total compensation for the CEOs of companies like Funko with market caps between US$400m and US$1.6b is about US$4.1m.

Funko's CEO took home a total compensation package worth US$2.4m in the year leading up to December 2021. That is actually below the median for CEO's of similarly sized companies. CEO remuneration levels are not the most important metric for investors, but when the pay is modest, that does support enhanced alignment between the CEO and the ordinary shareholders. Generally, arguments can be made that reasonable pay levels attest to good decision-making.

Is Funko Worth Keeping An Eye On?

Funko's earnings per share have been soaring, with growth rates sky high. The company can also boast of insider buying, and reasonable remuneration for the CEO. It could be that Funko is at an inflection point, given the EPS growth. For those attracted to fast growth, we'd suggest this stock merits monitoring. Even so, be aware that Funko is showing 2 warning signs in our investment analysis , you should know about...

There are plenty of other companies that have insiders buying up shares. So if you like the sound of Funko, you'll probably love this free list of growing companies that insiders are buying.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.