Yahoo Finance

Yahoo Finance Did Focus Minerals' (ASX:FML) Share Price Deserve to Gain 67%?

If you want to compound wealth in the stock market, you can do so by buying an index fund. But one can do better than that by picking better than average stocks (as part of a diversified portfolio). To wit, the Focus Minerals Limited (ASX:FML) share price is 67% higher than it was a year ago, much better than the market decline of around 0.6% (not including dividends) in the same period. If it can keep that out-performance up over the long term, investors will do very well! However, the longer term returns haven't been so impressive, with the stock up just 7.1% in the last three years.

View our latest analysis for Focus Minerals

With just AU$3,793,000 worth of revenue in twelve months, we don't think the market considers Focus Minerals to have proven its business plan. As a result, we think it's unlikely shareholders are paying much attention to current revenue, but rather speculating on growth in the years to come. It seems likely some shareholders believe that Focus Minerals will find or develop a valuable new mine before too long.

As a general rule, if a company doesn't have much revenue, and it loses money, then it is a high risk investment. There is usually a significant chance that they will need more money for business development, putting them at the mercy of capital markets to raise equity. So the share price itself impacts the value of the shares (as it determines the cost of capital). While some such companies go on to make revenue, profits, and generate value, others get hyped up by hopeful naifs before eventually going bankrupt. Focus Minerals has already given some investors a taste of the sweet gains that high risk investing can generate, if your timing is right.

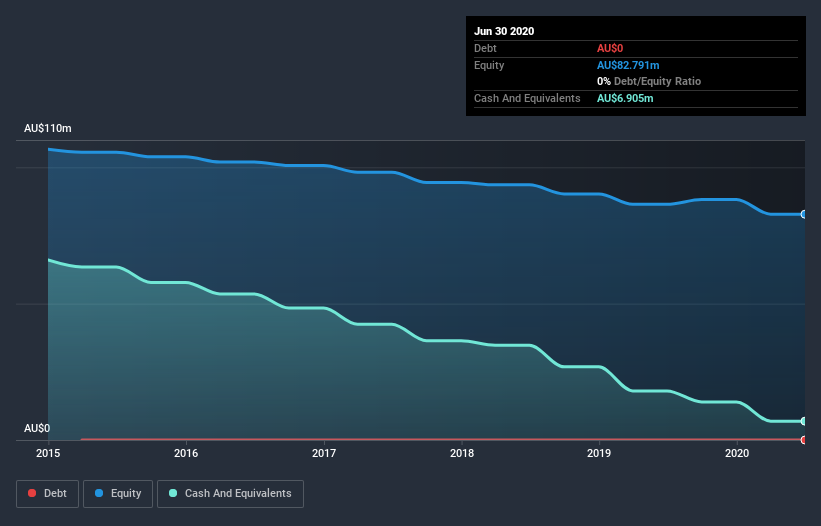

Our data indicates that Focus Minerals had AU$22m more in total liabilities than it had cash, when it last reported in June 2020. That makes it extremely high risk, in our view. So the fact that the stock is up 115% in the last year shows that high risks can lead to high rewards, sometimes. It's clear more than a few people believe in the potential. You can click on the image below to see (in greater detail) how Focus Minerals' cash levels have changed over time.

In reality it's hard to have much certainty when valuing a business that has neither revenue or profit. Given that situation, many of the best investors like to check if insiders have been buying shares. It's usually a positive if they have, as it may indicate they see value in the stock. Luckily we are in a position to provide you with this free chart of insider buying (and selling).

A Different Perspective

It's good to see that Focus Minerals has rewarded shareholders with a total shareholder return of 67% in the last twelve months. That's better than the annualised return of 1.4% over half a decade, implying that the company is doing better recently. Given the share price momentum remains strong, it might be worth taking a closer look at the stock, lest you miss an opportunity. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. For instance, we've identified 3 warning signs for Focus Minerals (1 is a bit unpleasant) that you should be aware of.

For those who like to find winning investments this free list of growing companies with recent insider purchasing, could be just the ticket.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on AU exchanges.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.