Yahoo Finance

Yahoo Finance Did Damstra Holdings' (ASX:DTC) Share Price Deserve to Gain 19%?

While Damstra Holdings Limited (ASX:DTC) shareholders are probably generally happy, the stock hasn't had particularly good run recently, with the share price falling 17% in the last quarter. But at least the stock is up over the last year. In that time, it is up 19%, which isn't bad, but is below the market return of 44%.

Check out our latest analysis for Damstra Holdings

Because Damstra Holdings made a loss in the last twelve months, we think the market is probably more focussed on revenue and revenue growth, at least for now. Generally speaking, companies without profits are expected to grow revenue every year, and at a good clip. That's because fast revenue growth can be easily extrapolated to forecast profits, often of considerable size.

Over the last twelve months, Damstra Holdings' revenue grew by 17%. We respect that sort of growth, no doubt. The share price gain of 19% in that time is better than nothing, but far from outlandish Its possible that shareholders had expected higher growth. However, if you can reasonably expect profits in the next few years, this stock might belong on your watchlist.

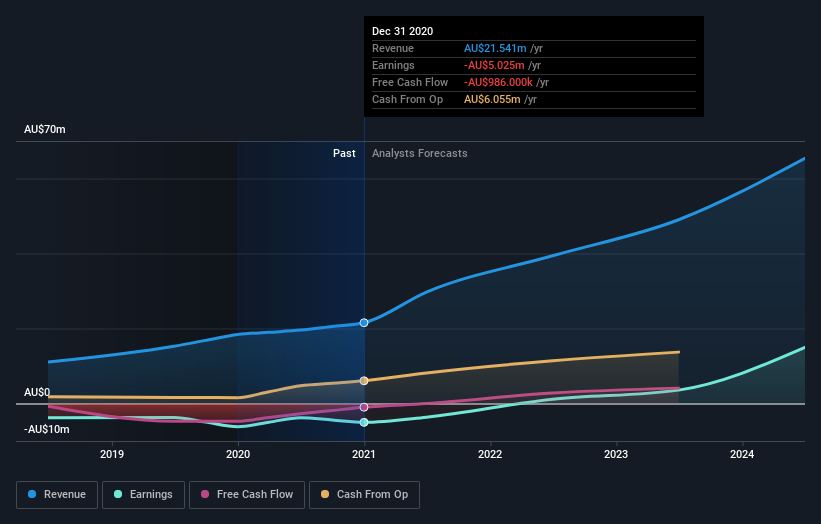

You can see how earnings and revenue have changed over time in the image below (click on the chart to see the exact values).

This free interactive report on Damstra Holdings' balance sheet strength is a great place to start, if you want to investigate the stock further.

A Different Perspective

Damstra Holdings shareholders have gained 19% for the year. While it's always nice to make a profit on the stock market, we do note that the TSR was no better than the broader market return of about 44%. The last three months haven't been great for shareholder returns, since the share price has trailed the market by 24% in the last three months. It might be that investors are more concerned about the business lately due to some fundamental change (or else the share price simply got ahead of itself, previously). I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. Take risks, for example - Damstra Holdings has 2 warning signs we think you should be aware of.

We will like Damstra Holdings better if we see some big insider buys. While we wait, check out this free list of growing companies with considerable, recent, insider buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on AU exchanges.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.