Yahoo Finance

Yahoo Finance CIRCOR International (NYSE:CIR) investors are sitting on a loss of 60% if they invested five years ago

We think intelligent long term investing is the way to go. But that doesn't mean long term investors can avoid big losses. For example the CIRCOR International, Inc. (NYSE:CIR) share price dropped 60% over five years. That is extremely sub-optimal, to say the least. And it's not just long term holders hurting, because the stock is down 36% in the last year. Furthermore, it's down 24% in about a quarter. That's not much fun for holders.

So let's have a look and see if the longer term performance of the company has been in line with the underlying business' progress.

View our latest analysis for CIRCOR International

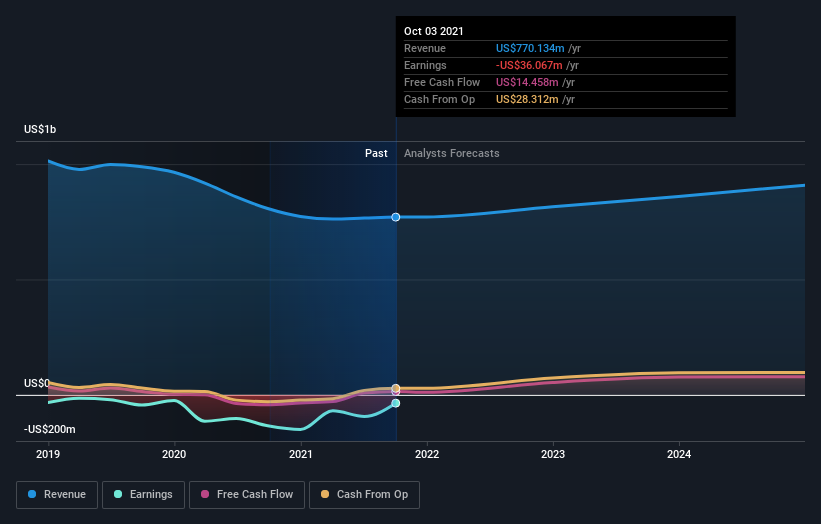

CIRCOR International wasn't profitable in the last twelve months, it is unlikely we'll see a strong correlation between its share price and its earnings per share (EPS). Arguably revenue is our next best option. When a company doesn't make profits, we'd generally expect to see good revenue growth. That's because it's hard to be confident a company will be sustainable if revenue growth is negligible, and it never makes a profit.

Over five years, CIRCOR International grew its revenue at 6.4% per year. That's a fairly respectable growth rate. The share price, meanwhile, has fallen 10% compounded, over five years. It seems probably that the business has failed to live up to initial expectations. A pessimistic market can create opportunities.

You can see below how earnings and revenue have changed over time (discover the exact values by clicking on the image).

We like that insiders have been buying shares in the last twelve months. Even so, future earnings will be far more important to whether current shareholders make money. You can see what analysts are predicting for CIRCOR International in this interactive graph of future profit estimates.

A Different Perspective

While the broader market gained around 15% in the last year, CIRCOR International shareholders lost 36%. However, keep in mind that even the best stocks will sometimes underperform the market over a twelve month period. Regrettably, last year's performance caps off a bad run, with the shareholders facing a total loss of 10% per year over five years. Generally speaking long term share price weakness can be a bad sign, though contrarian investors might want to research the stock in hope of a turnaround. It's always interesting to track share price performance over the longer term. But to understand CIRCOR International better, we need to consider many other factors. Even so, be aware that CIRCOR International is showing 2 warning signs in our investment analysis , and 1 of those is a bit concerning...

There are plenty of other companies that have insiders buying up shares. You probably do not want to miss this free list of growing companies that insiders are buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on US exchanges.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.