Yahoo Finance

Yahoo Finance Brown-Forman (BF.B) Q2 Earnings Miss Estimates, Sales Beat

Brown-Forman Corporation (BF.B) reported second-quarter fiscal 2023 results, wherein earnings missed the Zacks Consensus Estimate, while sales beat the same.

Sales also improved year over year, backed by the increased demand for its brands, mainly the resurgence of Jack Daniel’s Tennessee Whiskey, and growth across all geographic clusters. Meanwhile, earnings were affected by soft margin trends resulting from input cost inflation, higher supply-chain costs, and increased compensation and advertising expenses.

For the fiscal second quarter, earnings per share (EPS) of 47 cents declined 4% year over year and lagged the Zacks Consensus Estimate of 55 cents. The decline can be attributed to soft margins due to higher input costs, supply-chain headwinds, and increased compensation and advertising expenses, partly offset by sales growth and a lower effective tax rate.

Net sales of $1,094 million beat the Zacks Consensus Estimate of $1,089 million. The top line increased 10% year over year on a reported basis. On an organic basis, net sales were up 16% from the prior-year level. Sales benefited from strong consumer demand for its brands and sustained brand investments. BF.B is benefiting from recent acquisitions, product innovation and strategic relationships.

For the second quarter of fiscal 2023, Brown-Forman’s gross profit amounted to $613 million, improving 4% year over year. On an organic basis, the gross profit rose 13%.

Meanwhile, the gross margin contracted 330 basis points (bps) to 56%. The gross margin decline can be attributed to the impact of input cost inflation, elevated costs resulting from supply-chain disruptions and adverse currency rates. These were partly negated by a favorable price/mix and the removal of the EU and the U.K. tariffs on American whiskey.

SG&A expenses rose 9% year over year to $180 million and 15% on an organic basis, mainly on higher compensation-related expenses. Advertising expenses increased 16% year over year to $121 million for the fiscal second quarter.

On an organic basis, advertising expenses advanced 22%. This was driven by elevated marketing spends in the United States to back the growth of Jack Daniel’s Tennessee Whiskey, Herradura, the launch of the Jack Daniel’s Bonded series and Woodford Reserve.

The operating income declined 2% year over year to $313 million on a reported basis. The organic operating income increased 8%. The operating margin contracted 360 bps to 28.7% in the fiscal second quarter.

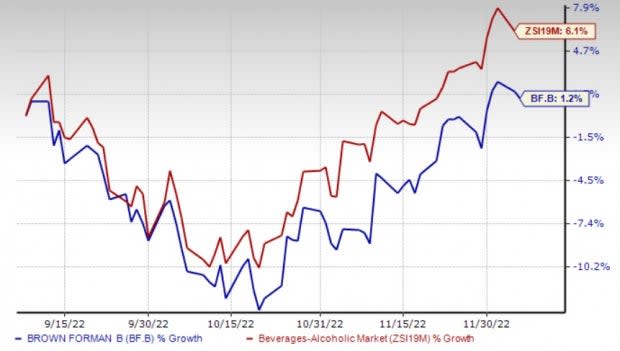

This Zacks Rank #3 (Hold) company’s shares have risen 1.2% in the past three months compared with the industry’s growth of 6.1%.

Image Source: Zacks Investment Research

Category-Wise & Channel-Wise Performance

For the first half of fiscal 2023, net sales increased 11% year over year to $2.1 billion and 17% on an organic basis. The rise was mainly driven by broad-based growth across all geographic regions and the Travel Retail channel on strong volume growth and rebuilding of distributor inventories.

Net sales for Jack Daniel’s family of brands were up 9% on a reported basis and 17% on an organic basis in the first half of fiscal 2023. The brand’s sales were driven by solid demand and increased prices in emerging markets, developed international markets and the Travel Retail channel.

The upside in sales was also driven by the resurgence of Jack Daniel’s Tennessee Whiskey, which reported sales growth of 9% and organic growth of 18%. Higher pricing and the estimated increase in distributor inventories also aided sales.

Further, sales benefited from the continued consumer interest in flavor and convenience, which boosted the performance of Jack Daniel’s Ready-to-Drink (RTD), Jack Daniel’s Tennessee Honey and Jack Daniel’s Tennessee Fire. Innovation contributed to sales growth through the launch of Jack Daniel’s Bonded series.

Premium bourbon brands reported sales growth of 39% and organic sales growth of 40% in the fiscal first half, driven by growth in Woodford Reserve and Old Forester, supported by higher volumes in the United States. An estimated rise in distributor inventories due to the easing of glass supply constraints also boosted sales for Woodford Reserve and Old Forester.

BF.B’s RTD category reported double-digit sales growth of 14% and organic sales growth of 20%. This was mainly driven by Jack Daniel’s RTDs and New Mix.

Jack Daniel’s RTDs/Ready-to-Pours benefited from gains in Australia and Germany, resulting in year-over-year sales growth of 9% and 15% on an organic basis. New Mix reported sales growth of 48% and organic sales growth of 46%, driven by market share gains in the RTD category in Mexico.

Brown-Forman’s tequila portfolio reported sales growth of 10% year over year and 11% on an organic basis. This was driven by volume growth in the United States for the el Jimador and Herradura brands.

Sales increased 9% on both reported and organic basis for the Herradura brand due to the positive impacts of an estimated increase in distributor inventories as supply constraints eased. el Jimador reported sales growth of 16% year over year and 18% on an organic basis.

The company’s overall sales in the United States advanced 11% on a reported and organic basis. The rise was driven by volume gains, a favorable mix and improved pricing across the portfolio. Higher volumes and pricing for Woodford Reserve and Jack Daniel’s Tennessee Whiskey were key drivers. These were partly negated by Korbel California Champagne, which witnessed higher pricing and lower volumes.

Meanwhile, the developed international market reported sales growth of 3%, with organic sales rising 14%. The improvement can be attributed to strong consumer demand. Volume gains from Jack Daniel’s Tennessee Whiskey and Jack Daniel’s RTDs mainly aided the results.

The emerging markets registered 14% net sales growth, whereas organic sales improved 27%. This was backed by the growth of Jack Daniel’s Tennessee Whiskey in Sub-Saharan Africa and Brazil, as well as New Mix in Mexico.

Net sales in the Travel Retail channel advanced 60% on a reported basis and 67% on an organic basis due to higher volumes for the majority of the portfolio as travel trends continued to rebound.

Balance Sheet & Cash Flow

The company ended the first half of fiscal 2023 with cash and cash equivalents of $1,087 million and long-term debt of $1,974 million. Its total shareholders’ equity was $3,040 million. As of Oct 31, 2022, BF.B generated $316 million in cash from operating activities.

Outlook

Despite the ongoing macroeconomic and geopolitical challenges, management anticipates continued growth for fiscal 2023. Brown-Forman expects strength in its brand portfolio and strong consumer demand and easing supply constraints to aid organic sales growth in fiscal 2023.

It anticipates organic sales growth in the high single digits for fiscal 2023 compared with the mid-single-digit growth expected earlier. The company expects the gross margin for fiscal 2023 to be consistent with the first half of fiscal 2023, wherein it reported a decline due to the effects of inflation, supply-chain disruption costs and currency headwinds.

Based on the aforementioned assumptions, Brown-Forman expects the organic operating income to increase in the high single digits. The effective tax rate is expected to be 22-23% for fiscal 2023. Capital expenditure is anticipated in the band of $190-$210 million.

Stocks to Consider

We have highlighted three better-ranked stocks from the Consumer Staples sector, namely Coca-Cola FEMSA KOF, PepsiCo Inc. PEP and Ambev ABEV.

Coca-Cola FEMSA produces, markets and distributes soft drinks throughout the metropolitan area of Mexico City in Southeastern Mexico and the metropolitan region in Buenos Aires, Argentina. KOF has a trailing four-quarter earnings surprise of 33.6%, on average. It currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today's Zacks #1 Rank stocks here.

Shares of Coca-Cola FEMSA have risen 8.4% in the past three months. The Zacks Consensus Estimate for Coca-Cola FEMSA’s current financial-year sales and earnings suggests growth of 15.6% and 6.2%, respectively, from the year-ago period's reported figures. KOF has an expected EPS growth rate of 10.3% for three to five years.

PepsiCo is one of the leading global food and beverage companies. It currently has a Zacks Rank #2 (Buy). The company has an expected EPS growth rate of 7.6% for three to five years. Shares of PEP have increased 5.2% in the past three months.

The Zacks Consensus Estimate for PepsiCo’s current financial-year sales and earnings per share suggests growth of 7.1% and 8%, respectively, from the year-ago period’s reported figures. PEP has a trailing four-quarter earnings surprise of 4.5%, on average.

Ambev is engaged in producing, distributing and selling beer, carbonated soft drinks, and other non-alcoholic and non-carbonated products in many countries across the Americas. ABEV currently has a Zacks Rank #2. Ambev has a trailing four-quarter earnings surprise of 4.4%, on average. Shares of ABEV have risen 2.7% in the past three months.

The Zacks Consensus Estimate for Ambev’s current financial-year sales and earnings suggests growth of 19.4% and 6.7%, respectively, from the year-ago period’s reported figures. ABEV has an expected EPS growth rate of 9.1% for three to five years.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

BrownForman Corporation (BF.B) : Free Stock Analysis Report

PepsiCo, Inc. (PEP) : Free Stock Analysis Report

Coca Cola Femsa S.A.B. de C.V. (KOF) : Free Stock Analysis Report

Ambev S.A. (ABEV) : Free Stock Analysis Report