Yahoo Finance

Yahoo Finance Bank of Queensland (ASX:BOQ) Will Pay A Larger Dividend Than Last Year At A$0.24

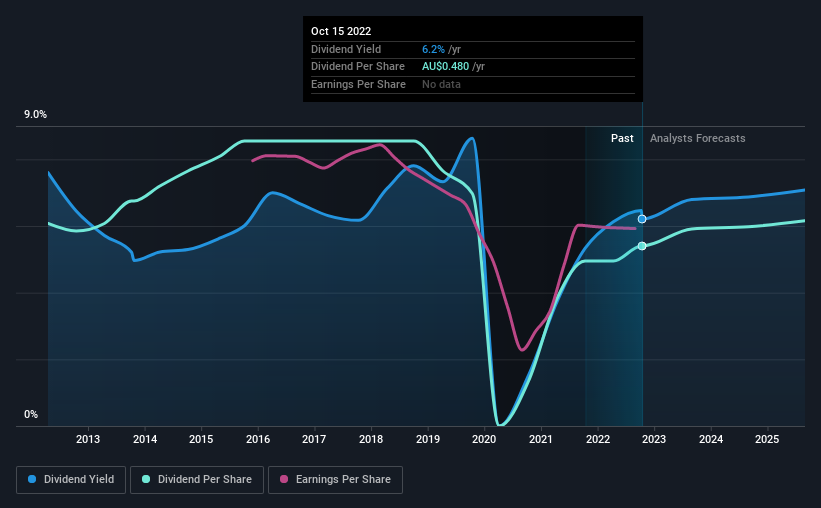

Bank of Queensland Limited (ASX:BOQ) has announced that it will be increasing its dividend from last year's comparable payment on the 17th of November to A$0.24. This will take the dividend yield to an attractive 6.2%, providing a nice boost to shareholder returns.

View our latest analysis for Bank of Queensland

Bank of Queensland's Earnings Will Easily Cover The Distributions

Impressive dividend yields are good, but this doesn't matter much if the payments can't be sustained.

Bank of Queensland has established itself as a dividend paying company with over 10 years history of distributing earnings to shareholders. Taking data from its last earnings report, calculating for the company's payout ratio shows 70%, which means that Bank of Queensland would be able to pay its last dividend without pressure on the balance sheet.

The next 3 years are set to see EPS grow by 15.5%. The future payout ratio could be 72% over that time period, according to analyst estimates, which is a good look for the future of the dividend.

Dividend Volatility

Although the company has a long dividend history, it has been cut at least once in the last 10 years. Since 2012, the dividend has gone from A$0.54 total annually to A$0.48. Doing the maths, this is a decline of about 1.2% per year. A company that decreases its dividend over time generally isn't what we are looking for.

Dividend Growth May Be Hard To Come By

With a relatively unstable dividend, it's even more important to evaluate if earnings per share is growing, which could point to a growing dividend in the future. Bank of Queensland has seen earnings per share falling at 6.3% per year over the last five years. If the company is making less over time, it naturally follows that it will also have to pay out less in dividends. However, the next year is actually looking up, with earnings set to rise. We would just wait until it becomes a pattern before getting too excited.

In Summary

Overall, this is probably not a great income stock, even though the dividend is being raised at the moment. The company hasn't been paying a very consistent dividend over time, despite only paying out a small portion of earnings. We would probably look elsewhere for an income investment.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. Just as an example, we've come across 2 warning signs for Bank of Queensland you should be aware of, and 1 of them can't be ignored. Is Bank of Queensland not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Join A Paid User Research Session

You’ll receive a US$30 Amazon Gift card for 1 hour of your time while helping us build better investing tools for the individual investors like yourself. Sign up here