Yahoo Finance

Yahoo Finance Automatic Data Processing, Inc. (NASDAQ:ADP) Just Released Its Third-Quarter Results And Analysts Are Updating Their Estimates

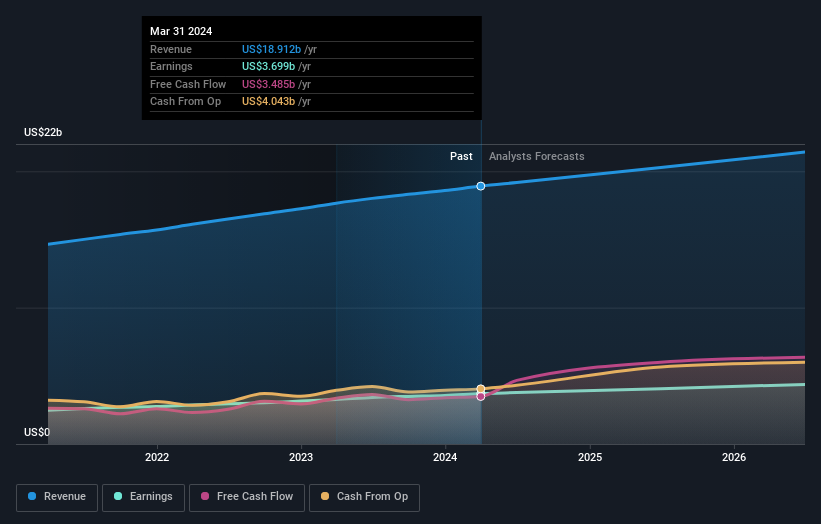

Last week saw the newest quarterly earnings release from Automatic Data Processing, Inc. (NASDAQ:ADP), an important milestone in the company's journey to build a stronger business. It was a credible result overall, with revenues of US$5.3b and statutory earnings per share of US$2.88 both in line with analyst estimates, showing that Automatic Data Processing is executing in line with expectations. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. We thought readers would find it interesting to see the analysts latest (statutory) post-earnings forecasts for next year.

Check out our latest analysis for Automatic Data Processing

Following the latest results, Automatic Data Processing's 17 analysts are now forecasting revenues of US$20.3b in 2025. This would be a satisfactory 7.2% improvement in revenue compared to the last 12 months. Per-share earnings are expected to grow 11% to US$10.00. In the lead-up to this report, the analysts had been modelling revenues of US$20.3b and earnings per share (EPS) of US$10.00 in 2025. So it's pretty clear that, although the analysts have updated their estimates, there's been no major change in expectations for the business following the latest results.

The analysts reconfirmed their price target of US$259, showing that the business is executing well and in line with expectations. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. There are some variant perceptions on Automatic Data Processing, with the most bullish analyst valuing it at US$282 and the most bearish at US$238 per share. Even so, with a relatively close grouping of estimates, it looks like the analysts are quite confident in their valuations, suggesting Automatic Data Processing is an easy business to forecast or the the analysts are all using similar assumptions.

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. We can infer from the latest estimates that forecasts expect a continuation of Automatic Data Processing'shistorical trends, as the 5.7% annualised revenue growth to the end of 2025 is roughly in line with the 6.4% annual growth over the past five years. Compare this with the broader industry, which analyst estimates (in aggregate) suggest will see revenues grow 5.6% annually. It's clear that while Automatic Data Processing's revenue growth is expected to continue on its current trajectory, it's only expected to grow in line with the industry itself.

The Bottom Line

The most obvious conclusion is that there's been no major change in the business' prospects in recent times, with the analysts holding their earnings forecasts steady, in line with previous estimates. They also reconfirmed their revenue estimates, with the company predicted to grow at about the same rate as the wider industry. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

With that in mind, we wouldn't be too quick to come to a conclusion on Automatic Data Processing. Long-term earnings power is much more important than next year's profits. We have forecasts for Automatic Data Processing going out to 2026, and you can see them free on our platform here.

You can also see our analysis of Automatic Data Processing's Board and CEO remuneration and experience, and whether company insiders have been buying stock.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.