Yahoo Finance

Yahoo Finance 5 Large Drug Stocks to Watch From a Thriving Industry

The drug and biotech sector has done well in 2023 despite macro-headwinds, with attractive valuations and strong fundamentals driving investor optimism for the sector. The large drugmakers are doing well, proving their resilience against recession, and are expected to remain strong.

Overall, innovation is likely to drive growth in the industry in 2023. M&A deals are also picking up, which shows growth. New drug launches and positive pipeline readouts are expected to keep investor focus on the sector. Among the large drugmakers, Eli Lilly LLY, J&J JNJ, Novo Nordisk NVO, Roche RHHBY and Novartis NVS are worth retaining in your portfolio.

Industry Description

The Zacks Large Cap Pharmaceuticals industry comprises some of the largest global companies that developmulti-million dollar drugs for a broad range of therapeutic areas like neuroscience, cardiovascular and metabolism, rare diseases, immunology, and oncology. Some of these companies also make vaccines, animal health, medical devices and consumer healthcare products. All these players invest millions of dollars in their product pipelines and line extensions of their marketed drugs. Continuous innovation is a defining characteristic of pharma companies and large drugmakers are constantly investing in drug development and the discovery of new medicines. Regular mergers and acquisitions and collaboration deals are other key features of large drug companies.

What's Shaping the Future of the Large-Cap Pharma Industry?

Innovation and Pipeline Success: For big drugmakers, innovation in their pipeline is a competitive necessity and key to top-line growth. Pharma companies are constantly striving to ramp up innovation and spending a significantly high portion of their revenues on R&D. Successful innovation and product line extensions in important therapeutic areas and strong clinical study results may act as important catalysts for these stocks.

Aggressive M&A & Collaboration Activity: The sector is characterized by aggressive M&A activity. Given that it takes several years and millions of dollars to develop new therapeutics from scratch, large pharmaceutical companies sitting on huge piles of cash regularly buy innovative small/mid-cap biotech companies to build out their pipelines. Also, the sloppy sales of mature drugs, dwindling in-house pipelines, government scrutiny of drug prices, and the emergence of big tech firms like Apple and Google in the healthcare industry whet the M&A appetite of large drugmakers. Fast-growing and lucrative markets such as oncology and cell and gene therapy are likely to remain focus areas for M&A activities. Also, collaborations and partnerships with smaller companies are in full swing. In less than half the year, two big acquisition announcements have already been made. Amgen has offered to buy Horizon Therapeutics for $27.8 billion while Pfizer has offered to buy cancer drugmaker, Seagen, for approximately $43 billion. However, the Federal Trade Commission (“FTC”) has filed a lawsuit in Federal Court to block the Amgen/Horizon Therapeutics deal as it believes the merger poses competitive issues.

Pipeline Setbacks & Other Headwinds: The failure of key pipeline candidates in pivotal studies and regulatory and pipeline delays can be setbacks for large drug companies and significantly hurt their share prices. Other headwinds for the industry include pricing and competitive pressure, generic competition for blockbuster treatments and a slowdown in sales of some of the most high-profile older drugs.

Macroeconomic Uncertainty: Higher interest rates, inflationary pressure from rising energy prices, significant economic volatility, supply chain pressure and the war in Europe are creating an uncertain macro environment and economic volatility.

Zacks Industry Rank Indicates Bright Prospects

The Zacks Large Cap Pharmaceuticals industryis a 12-stock group within the broader Medical sector. The group’s Zacks Industry Rank is basically the average of the Zacks Rank of all the member stocks.

The Zacks Large Cap Pharmaceuticals industry currently carries a Zacks Industry Rank #102, which places it in the top 41% of more than 250 Zacks industries. Our research shows that the top 50% of the Zacks-ranked industries outperform the bottom 50% by a factor of more than 2 to 1.

Before we present a few large drug stocks that are well-positioned to outperform the market based on a strong earnings outlook, let’s take a look at the industry’s performance and its current valuation.

Industry Versus S&P 500 & Sector

The industry has underperformed the S&P 500 but outperformed the Zacks Medical Sector this year so far.

Stocks in this industry have collectively declined 0.8% this year so far against the Zacks S&P 500 composite’s increase of 10.6%. The Zacks Medical Sector has declined 5.2%.

Year-to-Date Price Performance

Industry's Current Valuation

Based on the forward 12-month price-to-earnings (P/E), a commonly used multiple for valuing large pharma companies, the industry is currently trading at 16.94X compared with the S&P 500’s 18.76X and the Zacks Medical Sector's 21.99X.

Over the last five years, the industry has traded as high as 17.63X, as low as 13.31X and at a median of 14.98X, as the chart below shows.

Forward 12-Month Price-to-Earnings (P/E) Ratio

5 Large Drugmakers to Keep an Eye On

Roche: It has a strong presence in the oncology market. In particular, the company dominates the breast cancer space with strong demand for its HER2 franchise drugs.

Roche’s new drugs, namely Hemlibra (hemophilia), Ocrevus (multiple sclerosis), Evrysdi (spinal muscular atrophy) and Tecentriq (cancer) are doing well, making up for the declining demand for Roche’s COVID-19 products. The uptake of the new eye drug, Vabysmo (launched at the beginning of 2022) has been outstanding and it is already one of the top growth drivers for the company. Roche’s efforts to develop new drugs to combat the decline in legacy drugs are encouraging.

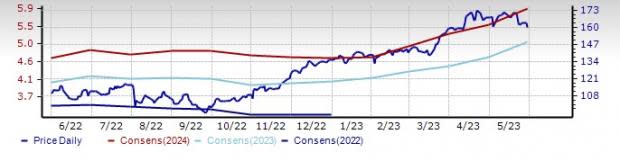

Roche has a Zacks Rank #2 (Buy). The Zacks Consensus Estimate for 2023 EPS has risen from $2.61 per share to $2.67 while that for 2024 has jumped from $2.83 per share to $2.89 over the past 60 days. The stock has risen 1.8% this year so far.

Price and Consensus: RHHBY

Novartis: It has a strong and diverse portfolio. Solid momentum in key brands like Entresto, Kesimpta, Zolgensma, Kisqali and Leqvio is fueling Novartis’ growth, offsetting the impact of rising generic competition. The pipeline progress is also impressive. The company has some promising candidates. Management’s focus on cost savings should boost the bottom line as well. The planned spin-off of the Sandoz unit remains on track for the second half of 2023. The spin-off will allow Novartis to focus on its core pharma business.

The Zacks Consensus Estimate for 2023 EPS has risen from $6.56 per share to $6.67 while that for 2024 has jumped from $7.05 per share to $7.22 over the past 60 days. Novartis is a #2 Ranked stock. This Swiss drugmaker’s stock has risen 6.4% this year so far.

Price and Consensus: NVS

Novo Nordisk: It has one of the broadest diabetes portfolios in the industry, with an extensive portfolio of insulin drugs and diabetes-related products. Semaglutide remains the growth engine for the company. It is approved as Ozempic pre-filled pen and Rybelsus oral tablet for type II diabetes and as Wegovy for weight management. Ozempic, Rybelsus, Xultophy and Saxenda have been helping the company maintain momentum. Label expansion of these existing drugs is expected to further boost sales. Novo Nordisk has also significantly stepped up its M&A activity in the past two years.

Novo Nordisk has a Zacks Rank #3 (Hold). Estimates for its 2023 earnings per share have increased from $4.48 to $5.07 over the past 60 days. Estimates for 2024 have jumped from $5.28 per share to $5.91 over the same timeframe. The stock has surged 18.1% this year so far.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Price and Consensus: NVO

Eli Lilly: It boasts a solid portfolio of core drugs in diabetes, autoimmune diseases and cancer. Its revenue growth is being driven by higher demand for drugs like Trulicity, Taltz and others. It is regularly adding promising new pipeline assets through business development deals. Lilly expects to launch four new medicines by 2023 end with Mounjaro for type II diabetes and cancer drug Jaypirca already launched. Mounjaro (tirzepatide) is already generating impressive sales, benefiting from strong demand trends. It is expected to be a key long-term top-line driver for Lilly as it has the potential to be approved for obesity and other diabetes-related diseases. Lilly expects the launch of mirikizumab, lebrikizumab and tirzepatide for obesity later in 2023.

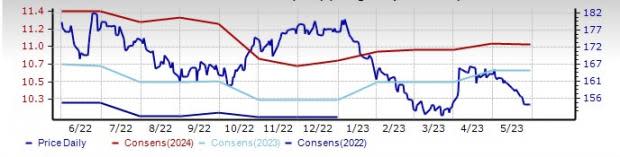

Lilly has a Zacks Rank #3. The Zacks Consensus Estimate for Lilly’s 2023 EPS has risen from $8.49 per share to $8.79 over the past 60 days while that for 2024 has increased from $11.58 per share to $12.08. The stock has risen 16.8% this year so far.

Price and Consensus: LLY

Johnson & Johnson: Its Pharma unit is performing at above-market levels. Growth in 2023 is expected to be driven by existing products like Darzalex, Tremfya, Erleada, Invega Sustenna and Uptravi, and also continued uptake from new launches, including Spravato, Carvykti and Tecvayli. The MedTech unit is showing improving trends, driven by recovery in surgical procedures and contribution from new products. J&J is making rapid progress with its pipeline and line extensions and has taken meaningful steps to resolve its talc and opioid litigation.

J&J has a Zacks Rank #3. The Zacks Consensus Estimate for this large drugmaker’s 2023 EPS has risen from $10.50 per share to $10.66 over the past 60 days while that for 2024 has jumped from $10.94 per share to $11.01. The stock has declined 12.6% this year so far.

Price and Consensus: JNJ

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Eli Lilly and Company (LLY) : Free Stock Analysis Report

Novartis AG (NVS) : Free Stock Analysis Report

Roche Holding AG (RHHBY) : Free Stock Analysis Report

Johnson & Johnson (JNJ) : Free Stock Analysis Report

Novo Nordisk A/S (NVO) : Free Stock Analysis Report