Yahoo Finance

Yahoo Finance These 4 Measures Indicate That Link Administration Holdings (ASX:LNK) Is Using Debt Extensively

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Link Administration Holdings Limited (ASX:LNK) makes use of debt. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for Link Administration Holdings

How Much Debt Does Link Administration Holdings Carry?

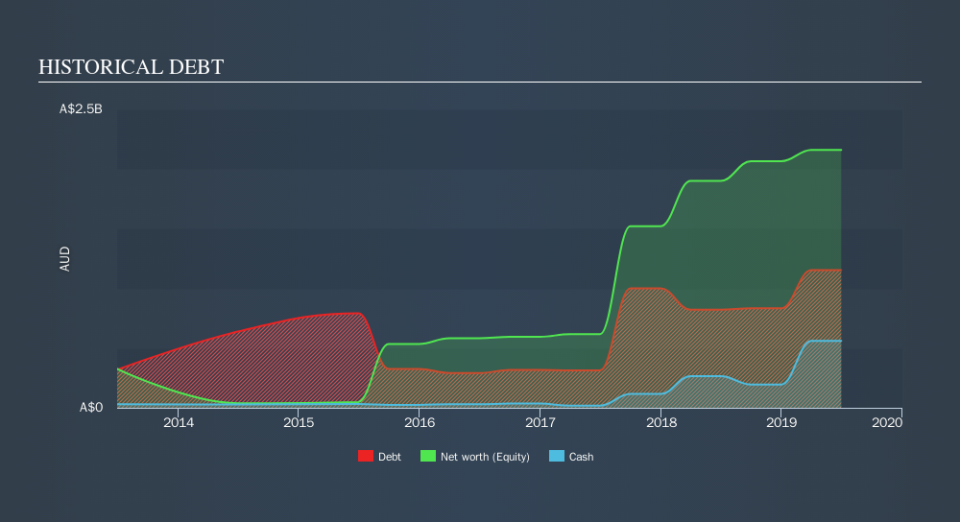

You can click the graphic below for the historical numbers, but it shows that as of June 2019 Link Administration Holdings had AU$1.15b of debt, an increase on AU$822.4m, over one year. On the flip side, it has AU$560.2m in cash leading to net debt of about AU$593.3m.

A Look At Link Administration Holdings's Liabilities

According to the last reported balance sheet, Link Administration Holdings had liabilities of AU$1.32b due within 12 months, and liabilities of AU$1.43b due beyond 12 months. Offsetting these obligations, it had cash of AU$560.2m as well as receivables valued at AU$177.1m due within 12 months. So its liabilities total AU$2.02b more than the combination of its cash and short-term receivables.

This deficit is considerable relative to its market capitalization of AU$2.97b, so it does suggest shareholders should keep an eye on Link Administration Holdings's use of debt. This suggests shareholders would heavily diluted if the company needed to shore up its balance sheet in a hurry.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

With a debt to EBITDA ratio of 2.3, Link Administration Holdings uses debt artfully but responsibly. And the alluring interest cover (EBIT of 7.5 times interest expense) certainly does not do anything to dispel this impression. Unfortunately, Link Administration Holdings's EBIT flopped 12% over the last four quarters. If that sort of decline is not arrested, then the managing its debt will be harder than selling broccoli flavoured ice-cream for a premium. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Link Administration Holdings's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So it's worth checking how much of that EBIT is backed by free cash flow. Over the most recent three years, Link Administration Holdings recorded free cash flow worth 66% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Our View

We feel some trepidation about Link Administration Holdings's difficulty EBIT growth rate, but we've got positives to focus on, too. To wit both its conversion of EBIT to free cash flow and interest cover were encouraging signs. We think that Link Administration Holdings's debt does make it a bit risky, after considering the aforementioned data points together. That's not necessarily a bad thing, since leverage can boost returns on equity, but it is something to be aware of. In light of our reservations about the company's balance sheet, it seems sensible to check if insiders have been selling shares recently.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.