Yahoo Finance

Yahoo Finance 3 Companies Estimated To Be Undervalued By Up To 46%

In a week marked by solid gains in U.S. stocks and a rebound from previous losses, the global markets have shown resilience despite mixed economic signals. With core inflation slightly higher than expected and treasury yields reaching year-to-date lows, investors are navigating an environment ripe for identifying undervalued opportunities. In this context, finding stocks that are estimated to be undervalued by up to 46% can offer significant potential for growth. Here we explore three such companies that stand out in the current market landscape.

Top 10 Undervalued Stocks Based On Cash Flows

Name | Current Price | Fair Value (Est) | Discount (Est) |

Zhongji Innolight (SZSE:300308) | CN¥115.94 | CN¥231.31 | 49.9% |

Kotobuki Spirits (TSE:2222) | ¥1719.00 | ¥3434.73 | 50% |

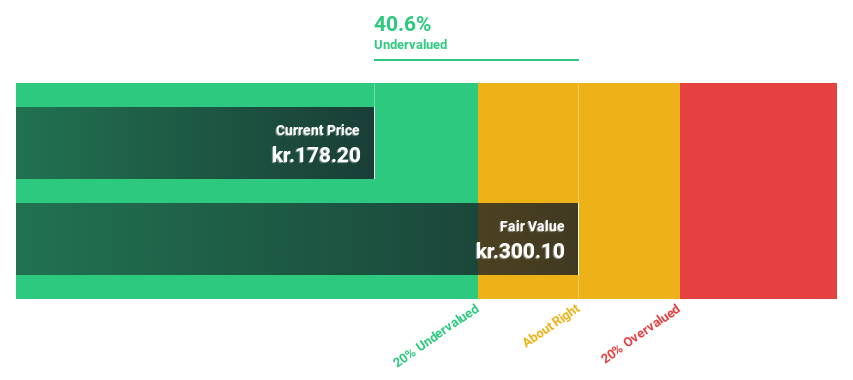

Plus Alpha ConsultingLtd (TSE:4071) | ¥2087.00 | ¥4159.36 | 49.8% |

Ohara (TSE:5218) | ¥1298.00 | ¥2594.34 | 50% |

Litium (OM:LITI) | SEK8.24 | SEK16.42 | 49.8% |

ChromaDex (NasdaqCM:CDXC) | US$3.55 | US$7.10 | 50% |

Shanghai INT Medical Instruments (SEHK:1501) | HK$28.20 | HK$56.15 | 49.8% |

Little Green Pharma (ASX:LGP) | A$0.085 | A$0.17 | 49.8% |

Hiconics Eco-energy Technology (SZSE:300048) | CN¥4.36 | CN¥8.72 | 50% |

Distribuidora Internacional de Alimentación (BME:DIA) | €0.0128 | €0.026 | 50% |

Below we spotlight a couple of our favorites from our exclusive screener.

Vestas Wind Systems

Overview: Vestas Wind Systems A/S designs, manufactures, installs, and services wind turbines in the United States, Denmark, and internationally with a market cap of DKK164.07 billion.

Operations: The company generates revenue through two primary segments: Service (€3.43 billion) and Power Solutions (€11.67 billion).

Estimated Discount To Fair Value: 39.9%

Vestas Wind Systems is trading at a significant discount to its estimated fair value, suggesting it may be undervalued based on cash flows. Despite recent financial challenges, including a net loss of €158 million in Q2 2024, the company is forecasted to grow earnings by 42.99% annually and become profitable within three years. Recent large-scale orders and long-term service agreements bolster its revenue outlook, supporting its potential for recovery and growth.

ASML Holding

Overview: ASML Holding N.V. develops, produces, markets, sells, and services advanced semiconductor equipment systems for chipmakers and has a market cap of approximately €288.48 billion.

Operations: ASML generates €25.44 billion in revenue from its Semiconductor Equipment and Services segment.

Estimated Discount To Fair Value: 16.2%

ASML Holding is trading 16.2% below its estimated fair value of €875.94, indicating potential undervaluation based on cash flows. Despite a decline in recent quarterly earnings, the company forecasts revenue growth of 16.2% annually and profit growth of 22.8%, outpacing the Dutch market. With significant insider selling recently and a highly volatile share price, caution may be warranted despite strong long-term earnings projections and high return on equity forecasts (52.9%).

Akeso

Overview: Akeso, Inc., a biopharmaceutical company with a market cap of HK$53.38 billion, researches, develops, manufactures, and commercializes antibody drugs.

Operations: Revenue from the research, development, production, and sale of biopharmaceutical products amounted to CN¥1.87 billion.

Estimated Discount To Fair Value: 46%

Akeso is trading 46% below its estimated fair value of HK$132.62, suggesting it may be undervalued based on cash flows. Despite recent shareholder dilution and a net loss of CNY 238.59 million for H1 2024, the company is forecast to grow revenue by 33.1% annually and become profitable within three years. Recent clinical trials show promising results for ivonescimab in treating various cancers, highlighting potential future revenue streams and long-term growth prospects.

Next Steps

Reveal the 920 hidden gems among our Undervalued Stocks Based On Cash Flows screener with a single click here.

Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Interested In Other Possibilities?

Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include CPSE:VWS ENXTAM:ASML and SEHK:9926.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com