Yahoo Finance

Yahoo Finance 3 Canadian E&P Stocks That Should be on Investors' Radar

The Zacks Oil and Gas - Exploration and Production - Canadian industry has lately been pegged back by investor skepticism toward risky assets and lower realizations, to go with uncertainties related to slowing global economic growth and inflationary pressures. Although macro challenges are leading to some demand concerns and fragility set against the backdrop of a widely forecast global downturn, we think the space still has certain things going for it. In the current environment, we advise investors to look at fundamentally solid companies like Canadian Natural Resources CNQ, Crescent Point Energy CPG and Baytex Energy BTE.

About the Industry

The Zacks Oil and Gas - US E&P industry consists of companies primarily based in the domestic market, focused on the exploration and production (E&P) of oil and natural gas. These firms find hydrocarbon reservoirs, drill oil and gas wells, and produce and sell these materials to be refined later into products such as gasoline, fuel oil, distillate, etc. The economics of oil and gas supply and demand is the fundamental driver of this industry. In particular, a producer’s cash flow is primarily determined by the realized commodity prices. In fact, all E&P companies' results are vulnerable to historically volatile prices in the energy markets. A change in realizations affects their returns and causes them to alter their production growth rates. The E&P operators are also exposed to exploration risks where drilling results are comparatively uncertain.

4 Key Investing Trends to Watch in the Oil and Gas - Canadian E&P Industry

Commodity Prices Down Significantly From 2022 Highs: Continued worries over the regional banking system and the fallout from the forced UBS-Credit Suisse tie-up means that volatile trading in crude is expected to continue for some time. In fact, the price of WCS crude — the Canadian benchmark — has come down sharply in recent months. After reaching a 14-year high of over $100 per barrel in March last year, the commodity has now tapered off to around $60. Natural gas has taken a beating, too, with abundant supply and weather woes limiting demand. The declining oil and gas prices are set to impact the fortunes of the domestic E&P players as they are now getting less for their products.

Inflationary Cost Pressures: Canadian energy companies have been experiencing rising production costs in the form of increased expenses related to steel, manufactured goods, services and labor. The inflationary environment, together with supply-chain tightness, is not only pushing costs higher but also affecting their capital programs. The scalation in expenses is also drowning out the benefits of any commodity price increase. In our view, the inflation-associated headwinds will continue to challenge growth and margin numbers with little chance of a quick resolution. This may lead to a rough road for oil/gas equities. In particular, worries about weaker energy demand due to the threat of recession might jeopardize the commodity’s ascent.

Lack of Pipeline Availability: Energy consultant IHS Markit sees oil production in Canada surging by some 900,000 barrels per day during 2020-2030. Despite this impressive output growth, the country's exploration and production sector has remained out of favor, primarily due to the scarcity of pipelines. This has forced producers to give away their products in the United States — Canada’s major market — at a discounted rate. Following U.S. President Joe Biden’s revocation of TC Energy’s contentious Keystone XL pipeline and the company’s subsequent termination of the project, Canadian oil sands producers will have to wait a little longer for the takeaway capacity issue to be resolved.

Companies Prioritizing Returning More Cash to Shareholders: The sharp increase in crude prices last year allowed the Canadian upstream operators to deliver a solid financial performance. In particular, cash from operations is on a sustainable path, with revenues improving and companies slashing capital expenditures from the pre-pandemic levels amid higher commodity realizations. To put it simply, the environment of strong prices in 2022 helped the E&P firms to generate significant “excess cash,” which they intend to use to boost investor returns. In fact, more and more energy companies are allocating their increasing cash pile by way of dividends and buybacks to pacify the long-suffering shareholders.

Zacks Industry Rank Indicates Bearish Outlook

The Zacks Oil and Gas - Canadian E&P is an eight-stock group within the broader Zacks Oil - Energy sector. The industry currently carries a Zacks Industry Rank #191, which places it in the bottom 24% of more than 250 Zacks industries.

The group’s Zacks Industry Rank, which is basically the average of the Zacks Rank of all the member stocks, indicates challenging near-term prospects. Our research shows that the top 50% of the Zacks-ranked industries outperforms the bottom 50% by a factor of more than 2 to 1.

The industry’s position in the bottom 50% of the Zacks-ranked industries is a result of a negative earnings outlook for the constituent companies in aggregate. Looking at the aggregate earnings estimate revisions, it appears that analysts are becoming pessimistic about this group’s earnings growth potential. While the industry’s earnings estimates for 2023 have gone down 29.8% in the past year, the same for 2024 have fallen 50.9% over a similar timeframe.

Despite the dim near-term prospects of the industry, we will present a few stocks that you may want to consider for your portfolio. But it’s worth taking a look at the industry’s shareholder returns and current valuation first.

Industry Lags Sector & S&P 500

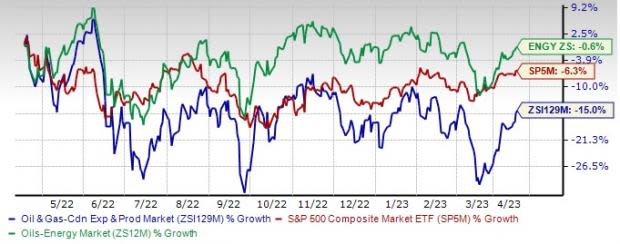

The Zacks Oil and Gas - Canadian E&P has fared worse than the broader Zacks Oil - Energy sector as well as the Zacks S&P 500 composite over the past year.

The industry has gone down 15% over this period compared with the broader sector’s decrease of 0.6%. Meanwhile, the S&P 500 has lost 6.3%.

One-Year Price Performance

Industry's Current Valuation

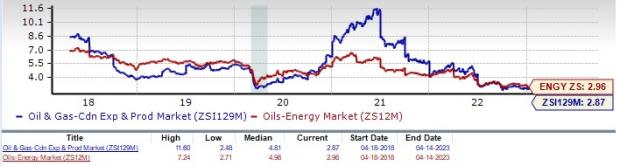

Since oil and gas companies are debt-laden, it makes sense to value them based on the EV/EBITDA (Enterprise Value/ Earnings before Interest Tax Depreciation and Amortization) ratio. This is because the valuation metric takes into account not just equity but also the level of debt. For capital-intensive companies, EV/EBITDA is a better valuation metric because it is not influenced by changing capital structures and ignores the effect of non-cash expenses.

On the basis of the trailing 12-month EV/EBITDA ratio, the industry is currently trading at 2.87X, significantly lower than the S&P 500’s 12.65X. It is also below the sector’s trailing-12-month EV/EBITDA of 2.96X.

Over the past five years, the industry has traded as high as 11.60X, as low as 2.48X, with a median of 4.81X, as the chart below shows.

Trailing 12-Month Enterprise Value-to EBITDA (EV/EBITDA) Ratio (Past Five Years)

Stocks to Watch For

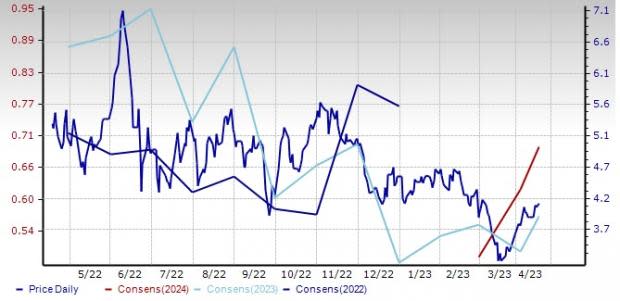

Baytex Energy: An energy producer based in Western Canada, Baytex focuses on a high-quality and diversified oil portfolio across multiple plays, spanning Peace River, Duvernay, Lloydminster and Viking. The company is also active in the Eagle Ford shale. Banking on its strong execution and disciplined capital allocation, BTE is on track to generate substantial free cash flow in this commodity upcycle. Baytex is also relentlessly working to improve its leverage ratios and enhance shareholder returns.

Headquartered in Calgary, Alberta, BTE delivered a 46.2% beat in Q4. Over the past 60 days, Baytex saw the Zacks Consensus Estimate for 2023 move up 7.5%. BTE, carrying a Zacks Rank #1 (Strong Buy), has seen its stock go down 23.3% in a year. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

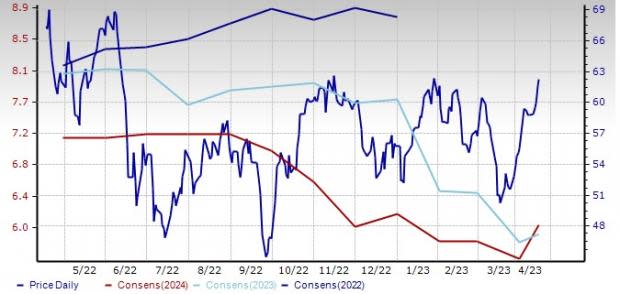

Price and Consensus: BTE

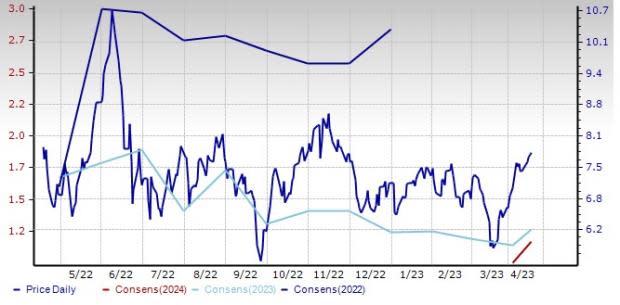

Crescent Point Energy: This Calgary-based company, whose operations are primarily concentrated in southwest and southeast Saskatchewan, carries a Zacks Rank #2 (Buy). Crescent Point, which acquired Shell’s Alberta assets for C$900 million last year, counts operational excellence and prudent cost management as its strength. With a low-risk drilling inventory of long-life assets and strong market access, CPG is also making progress on balance sheet strength and shareholder return initiatives.

Over the past 60 days, Crescent Point saw the Zacks Consensus Estimate for 2023 move up 7%. The company enjoys a Value and Gowth Style Score of A each to help it round out with a VGM Score of A. Valued at around $4.3 billion, CPG has edged down 1.7% in a year.

Price and Consensus: CPG

Canadian Natural Resources: This Calgary-based energy major boasts a diversified portfolio of crude oil (heavy as well as light), natural gas, bitumen and synthetic crude oil. CNQ’s balanced and diverse production mix facilitates long-term value and reduces the risk profile, thereby lending its results a high level of stability. Lower capital expenditure needs, accretive acquisitions and improving operational efficiencies are the other positives in the Canadian Natural story, which allowed the company to generate a significant free cash flow of C$10.9 billion (post capital spending and dividends) in 2022.

Notably, CNQ beat the Zacks Consensus Estimate for earnings in three of the last four quarters. The company has a trailing four-quarter earnings surprise of 10.5%, on average. Canadian Natural, with a Zacks Rank #3 (Hold), has seen its shares lose 7.8% in a year.

Price and Consensus: CNQ

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Canadian Natural Resources Limited (CNQ) : Free Stock Analysis Report

Baytex Energy Corp (BTE) : Free Stock Analysis Report

Crescent Point Energy Corporation (CPG) : Free Stock Analysis Report